What Credit Score Do I Need to Buy a Car? A Calm UK Guide

If you’re hoping to buy a car on finance, it’s natural to want a target score. In the UK, it’s calmer than that: lenders don’t all use the same score, and they focus on your report details and affordability. Here’s how to sense-check your chances and what to do if you’re applying soon.

Quick Answer

What credit score do I need to buy a car?

In the UK, there isn’t one magic credit score needed to buy a car. Car finance lenders usually look at your credit report (recent payment history, how much credit you’re using, and any serious negative markers) plus affordability (income and regular outgoings).

A higher score band can help you access more deals, but it’s common to be accepted with a lower score if your report is stable and the monthly payment is comfortably affordable.

For a clear overview of how credit scores and reports work in the UK, MoneyHelper is a good starting point: credit scores and credit reports.

Why there’s no single “required score” (and what to use instead)

When you search what credit score do I need to buy a car, you’re usually hoping for a pass mark. Two things make that tricky in the UK:

- Score ranges differ across Experian, Equifax and TransUnion.

- Lenders don’t all use the score you see in an app. Many use credit reference agency data plus their own internal scorecards.

A more useful way to sense-check your chances is to look at:

- Your score band (fair / good / excellent) on whichever agency you’re checking

- Any adverse markers (missed payments, defaults, CCJs) and how recent they are

- Your affordability picture (what the monthly payment looks like compared with your regular outgoings)

If you’d like a calm refresher on why the number can differ across agencies, see Average Credit Score UK: What’s Normal and What to Do Next.

What car finance lenders usually check

Car finance decisions tend to come down to two questions:

- Creditworthiness: does your report suggest you repay reliably?

- Affordability: does the payment fit your budget (including existing credit commitments)?

That’s why two people with the same score can get different outcomes: the report details and income/outgoings matter.

The report items that most often move the needle

- Missed payments (recency matters): a late payment last month is viewed differently to one from years ago.

- Credit utilisation: high card balances close to the statement date can make you look “stretched” even if you pay in full later.

- Recent hard searches: lots of applications in a short window can look like stress.

- Stability signals: consistent address details and being on the electoral register (if eligible).

If your score has suddenly dipped right before you’re planning to apply, this checklist helps you find the reason quickly: Why Has My Credit Score Gone Down? A Calm UK Checklist.

PCP vs hire purchase vs personal loan: does it change the “needed score”?

It can change the shape of the decision, but not the fundamentals. All credit products look at creditworthiness and affordability. What tends to differ is the size of the monthly payment, the deposit, and how sensitive the lender is to recent issues.

PCP

Often a lower monthly payment, with an optional final payment. Lenders still assess affordability and your report, but the structure can make affordability checks feel stricter for some people.

Hire Purchase

Straightforward fixed payments to own the car at the end. If the payment is comfortably affordable, this can be simpler to budget for.

Personal Loan

You own the car outright. Rates can be competitive for strong profiles, but it’s still a full credit application and your rate depends on the lender’s criteria.

Before you sign anything, read the agreement carefully and ask the provider what happens if your circumstances change. If you want a neutral explainer of car finance types, MoneyHelper has practical guides across common options.

Soft checks vs hard checks: what happens when you apply

People often avoid shopping around because they’re worried about damaging their score. The calm approach is to get clear on what kind of search is happening.

- Soft searches are typically used for “eligibility” style checks and don’t impact your score in the same way a full application can.

- Hard searches are usually recorded when you submit a full application for finance.

Before you let a dealership or broker proceed, ask: “Is this a soft search or a hard search?” If you’re not ready, it’s OK to pause.

14-Day Tidy-Up

A practical 14-day plan before you apply for car finance

This is not about chasing a perfect number. It’s about making your file easy to understand and your budget easy to defend.

- Check your credit reports. Look for missed payments, wrong balances, or accounts you don’t recognise.

- Fix identity details. Make sure your address matches across key accounts and register to vote if eligible.

- Reduce utilisation where you can. If possible, bring card balances down before the next statement date.

- Keep your file quiet. Avoid applying for other credit (cards, BNPL, mobiles) until the car is sorted.

- Run the affordability maths. If the monthly payment would make you rely on credit for normal life, it’s too tight.

- Prepare documentation. If asked, have payslips, bank statements, and proof of address ready.

If you’re comparing options, it can help to narrow to one or two realistic deals first, rather than submitting lots of applications.

A quick “is this car worth it?” check (in hours, not just pounds)

Credit checks matter, but so does what happens after you’re approved. A car payment that’s technically affordable can still feel heavy if it squeezes your month.

One practical habit: translate the monthly payment into your time.

- If your car payment is £320 per month and you take home £16 per hour, that’s 20 hours of work each month.

- If insurance, fuel, and maintenance add another £180, that’s another 11.25 hours.

Seeing the commitment in hours makes it easier to decide whether you want that trade-off, or whether a different car (or a slightly larger deposit) would feel calmer.

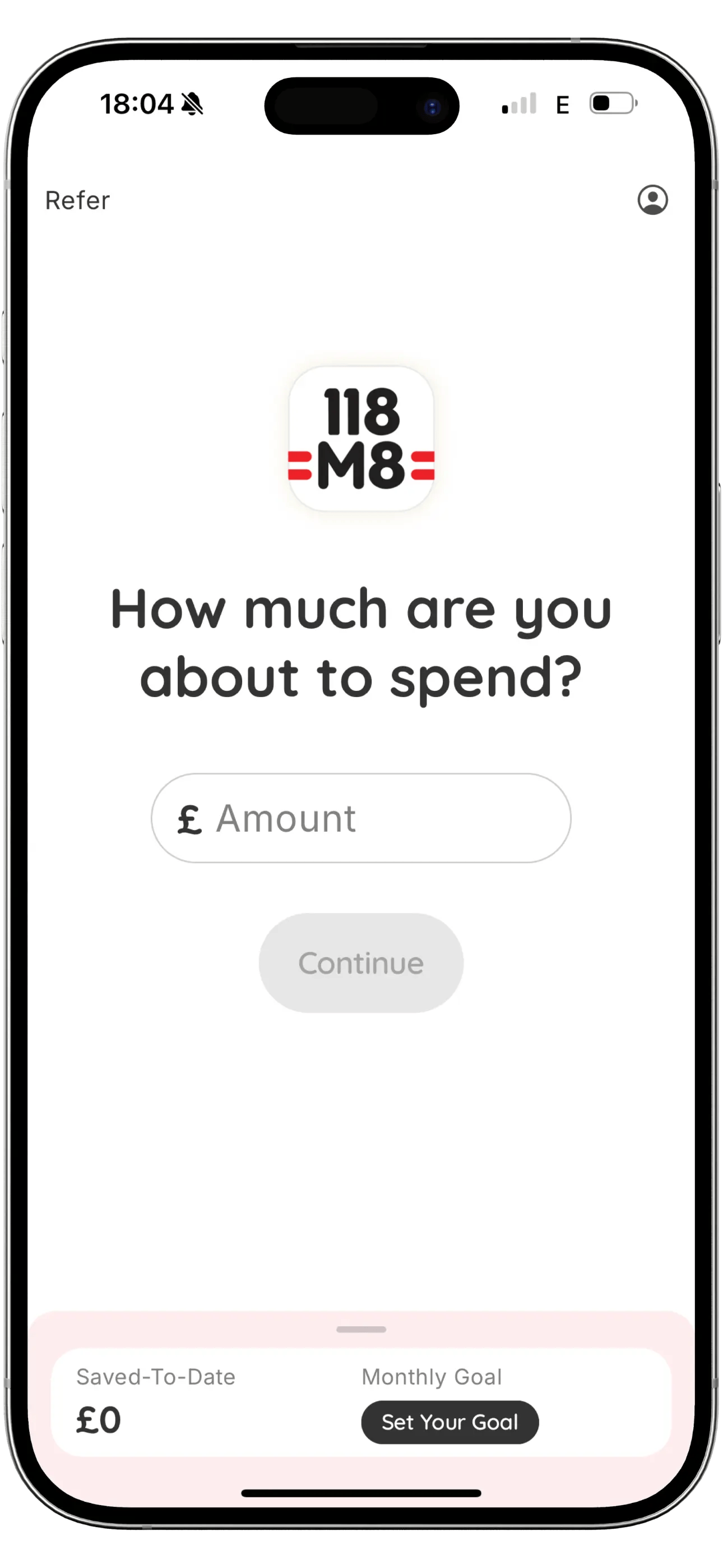

About 118M8: keep car money decisions calm

Buying a car is a big commitment. 118M8 helps with the everyday part by turning prices into hours worked, so you can pause before you spend and keep your budget steady while you’re preparing for finance.

- Sense-check purchases in time, not just pounds

- Use “Sleep on it” for a 24-hour decision pause

- Track what you didn’t spend and keep momentum

More calm guides: Credit Scores · Subscriptions · Blog home

Frequently Asked Questions

What credit score do I need to buy a car in the UK?

There isn’t one universal number. Lenders look at the underlying credit report and affordability. Use your score band (fair, good, excellent) as a guide, then pay close attention to recent missed payments, utilisation, and lots of recent applications.

Can I get car finance with a poor credit score?

Sometimes, yes. The trade-off is often a higher APR, larger deposit, or tighter terms. If you’re close to applying, focus on stability: keep payments on time, reduce utilisation where possible, and avoid submitting lots of applications.

Do dealerships run a hard credit check for car finance?

Many full applications involve a hard search, but some lenders offer eligibility checks that use a soft search first. Ask what type of search will be recorded before you proceed.

Is PCP harder to get than hire purchase?

Not always. It depends on the lender and your affordability. PCP can have lower monthly payments but a different structure, so the “best” option is often the one that leaves your budget feeling comfortable month to month.

How can I improve my chances of car finance quickly?

In the two weeks before you apply, focus on accuracy and calm: check your reports, fix identity details, reduce utilisation before statement dates, keep applications to a minimum, and make sure the payment fits your budget without relying on credit for normal spending.