No Deposit Car Insurance: What UK Drivers Need to Know

If you are searching for no deposit car insurance, you are usually trying to solve a cash-flow problem, not a technical insurance problem. In the UK, this phrase almost always means a policy with low or no upfront payment and monthly instalments after that. The key is understanding what you are really buying, what it costs over the year, and whether the easier start ends up costing far more than you expected.

A calm 10-minute check before you buy monthly cover

- Check what “no deposit” really means on the quote. It usually means monthly payments, not free cover.

- Write down the total yearly cost, not just the first month.

- Compare the same cover level, excess, mileage, drivers, and add-ons.

- Look for premium finance charges or a higher total payable when paying monthly.

- Check the start date carefully so you do not leave the car uninsured.

- Before you click buy, convert the total into hours worked so the number feels real.

The aim is not to shame monthly payments. It is to make sure the easier start does not quietly turn into an expensive year.

What no deposit car insurance usually means

No deposit car insurance is one of those phrases that sounds clearer than it really is. In the UK, it usually does not mean you get insured without paying anything upfront. It normally means the insurer or broker lets you spread the cost over monthly instalments, sometimes with a very small first payment and sometimes with no larger initial lump sum at all.

Compare the Market puts it bluntly: there is effectively no true car insurance with no deposit in the sense of getting cover without paying for it. What people usually mean is cover paid monthly rather than annually. That distinction matters because the monthly route can cost more overall once premium finance is added.

If you came here hoping for a hidden zero-upfront loophole, the calmer answer is simpler: there may be low-upfront or spread-cost options, but the bill still exists. The smart move is to compare the full-year cost and decide whether the cash-flow relief is worth it.

The simple answer

Key Point

Why so many drivers search for it

Usually, this search is about timing and pressure. Car insurance is legally required if you use your vehicle on roads or in public places in the UK, and if the vehicle is not insured and not declared off road with a SORN, you can face penalties. That means many drivers are not shopping casually. They are up against a renewal date, a new-car purchase, or a cash squeeze. GOV.UK is clear that you must insure a vehicle you use on the road, and that uninsured vehicles that are not SORN can trigger enforcement.

That urgency makes “no deposit car insurance” feel attractive for obvious reasons:

- You need cover now, but do not want a large upfront hit.

- You want to keep cash back for fuel, repairs, or other bills.

- You are trying to keep the monthly budget steady instead of absorbing one big annual cost.

None of that is irrational. The risk is simply that urgency narrows your attention to the first payment and hides the total cost of the deal.

Is monthly car insurance more expensive overall?

Often, yes. Paying monthly commonly involves premium finance. That is the credit arrangement used to spread the premium over the year. The Financial Conduct Authority said in February 2026 that nearly half of motor and home insurance policies in 2023 were paid monthly, often because customers could not afford annual payments. The FCA also said regulatory attention had pushed premium-finance rates down, saving customers money compared with earlier years. That is good news, but it does not mean monthly and annual prices are the same.

In other words, monthly payments may be getting fairer, but they can still cost more than paying in one go. This is exactly why the phrase “no deposit car insurance” can mislead. It frames the choice around the opening move, while the real decision is about the total cost across 12 months.

How to compare no deposit car insurance properly

The cleanest way to compare quotes is to turn every option into the same simple question: What will this policy cost me in total over the year for the same cover?

That means ignoring the marketing label for a moment and lining up the real details:

- Third party, third party fire and theft, or comprehensive

- Compulsory and voluntary excess

- Main driver and named drivers

- Annual mileage

- Where the car is kept overnight

- Breakdown, legal cover, courtesy car, and other add-ons

- Total amount payable over 12 months

If one quote says £84 a month and another says £91 a month, the first one is not automatically better. One may have a much higher excess. Another may have more useful cover. Another may simply be quoting on slightly different details.

What to compare on a no deposit car insurance quote

| Check | Why it matters | What to watch for |

|---|---|---|

| Monthly payment | It affects cash flow right now. | A low first month can distract you from the yearly cost. |

| Total yearly cost | This is the truest price comparison. | Monthly plans can cost more once finance is added. |

| Excess | This affects what you pay if you claim. | Cheaper premiums can hide a painful excess. |

| Add-ons | They change both price and value. | You may be paying for extras you do not need. |

| Your details | Quotes must match your real situation. | Different mileage or parking answers make comparisons unreliable. |

The calm rule is simple: compare like-for-like and judge the total payable, not just the headline monthly number.

Can you really get zero upfront car insurance?

Sometimes you may see quotes or brokers talk about zero deposit, nothing upfront, or pay monthly from the start. That can happen, but the important question is not whether the first payment is called a deposit. The important question is whether the policy cost is being spread and financed.

That is why it helps to think in plain English:

- Annual payment means one bigger hit now, often a lower total price.

- Monthly payment means an easier start, often a higher total price.

- “No deposit” marketing usually sits in the second group.

So yes, you may find quotes that do not ask for a larger upfront chunk. But that does not make them cheaper. It just changes how the cost shows up.

When paying monthly can still make sense

There is no point pretending annual payment is always realistic. For plenty of drivers, it is not. If the choice is between manageable monthly payments and the risk of delaying cover, monthly payment can be the right move. The legal and practical need for insurance is real, and a cash-flow-friendly option may simply fit your life better.

Paying monthly can make sense when:

- You cannot comfortably afford the annual premium without creating other problems.

- You need cover immediately and the alternative is going uninsured.

- You have compared the total payable and decided the extra cost is worth the flexibility.

The key is to make that trade-off on purpose. If you are choosing monthly because it is genuinely the best fit for your cash flow, that is a rational decision. If you are choosing it because the quote layout hid the true yearly cost, that is a problem.

What to do if the annual payment is out of reach

If you want the cash-flow benefit of no deposit car insurance but not the worst possible price, there are still practical ways to improve the outcome.

Start with the basics that usually move quotes:

- Check mileage is realistic, not guessed.

- Remove unnecessary add-ons before you touch excess.

- Compare 3 to 5 like-for-like quotes rather than stopping at the first monthly option.

- Look at renewal timing, because earlier shopping can lower quotes for some drivers.

- Think ahead to your next car if insurance cost keeps hurting your budget.

For broader help with quote timing, read Best Time to Renew Car Insurance in the UK. If the bigger problem is the car itself, Cheapest Cars to Insure: UK Picks and a Calm Checklist can help you avoid repeating the same pain next time.

No deposit car insurance vs annual payment

Monthly no-deposit-style cover compared with annual payment

| Approach | Best part | Main trade-off |

|---|---|---|

| Pay annually | Often lower total cost over the year. | Bigger hit to cash flow upfront. |

| Pay monthly | Smaller payments that are easier to fit into a monthly budget. | Often higher total payable because of premium finance. |

| Low or zero upfront monthly option | Less pressure at the start of the policy. | Can look cheaper than it really is if you only focus on month one. |

This is a budgeting comparison, not a promise of exact pricing. Always check your own quote documents carefully.

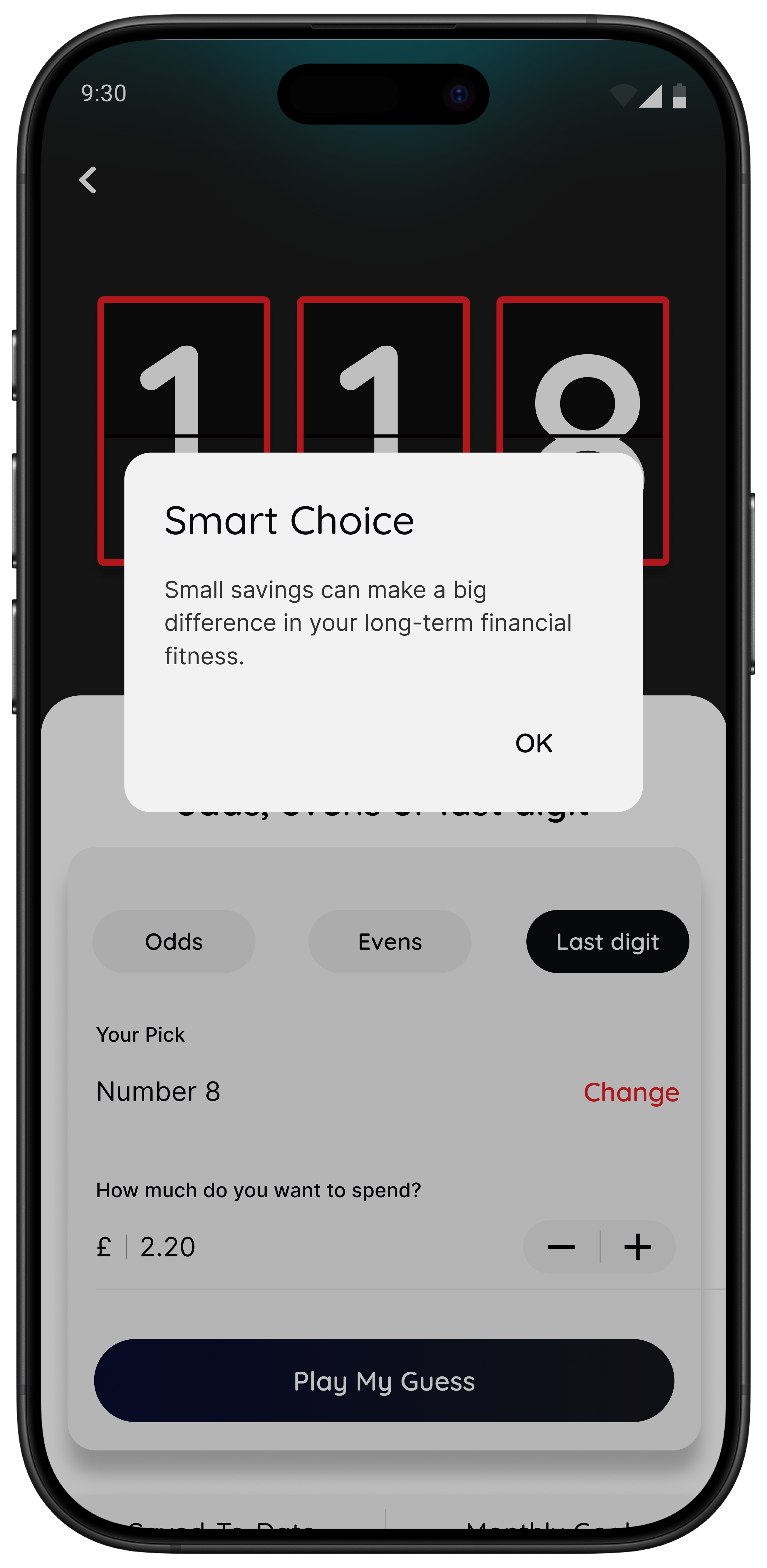

Quick check what does this policy cost in hours worked

One reason annual insurance decisions go fuzzy is that the numbers feel abstract. A monthly quote can feel small enough to ignore, even when the total is not. Converting the policy into hours worked can make the trade-off feel much clearer.

Quick Check

What does this policy cost in hours?

Enter the full yearly cost if you want the clearest comparison between annual and monthly options.

That policy costs you

0.0 hours

Spread across the year

That’s 0.0 hours of take-home time per month.

This is a decision tool, not financial advice. It helps you judge whether the monthly convenience is worth the total time cost.

Common mistakes that make no deposit quotes look better than they are

The phrase itself creates the first trap, but there are a few others worth watching for:

- Comparing monthly payment but not total payable.

- Missing optional extras bundled into the quote.

- Choosing a high excess just to force the premium down.

- Leaving the search until the final days and accepting the first workable option.

- Ignoring whether the car must be insured or SORN if you are tempted to delay the decision.

MoneyHelper’s car insurance guide is useful for the basics of cover types and excess, while GOV.UK explains the legal insurance requirement and when SORN applies. Together, they help separate the legal must-do from the pricing choice.

A calm script for choosing between two monthly quotes

If you are stuck between two sensible options, keep the decision plain:

- Which one is cheaper over the full year?

- Which one has the excess I could actually afford?

- Which one includes only the extras I would genuinely use?

If one quote wins two out of three, you probably have your answer. If they are still very close, the decision may not need more overthinking. It may just need a short pause so you do not buy under pressure.

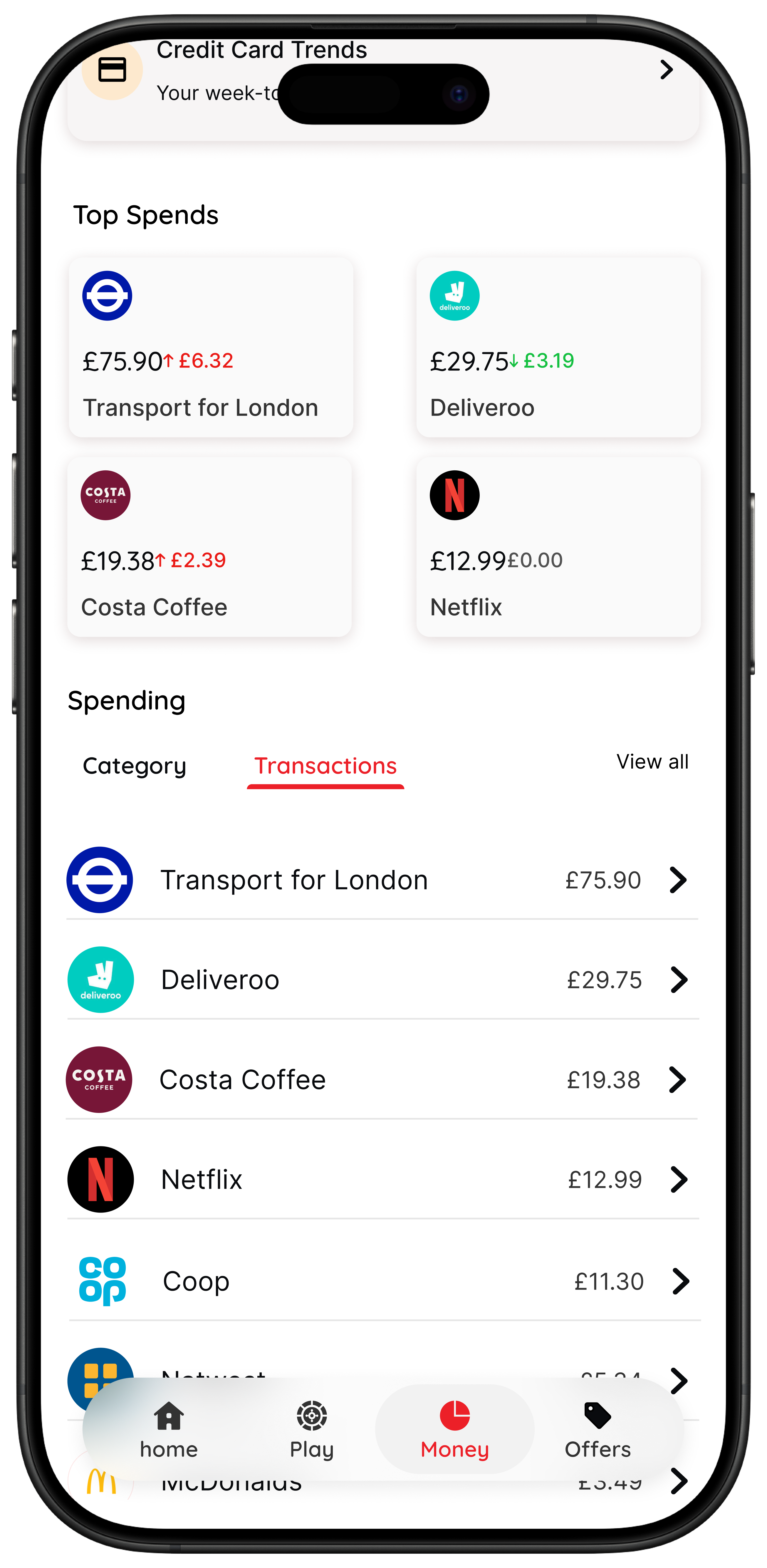

How 118M8 can help with car insurance decisions

No deposit car insurance is exactly the sort of search that happens when pressure is high and patience is low. That is where 118M8 fits.

It is not an insurance app. It is a financial fitness mate for the moment before you commit.

- Spot it: see spending patterns more clearly if you already use 118 118 Money products.

- Clock it: use Wait to turn the total premium into hours worked.

- Pause it: use Sleep on it when the quote is good enough to consider but too important to rush.

- Choose it: use Number Generator if you are stuck between two reasonable options and need a neutral pause, not a lecture.

About 118M8

A calmer way to handle the money moment before you buy

118M8 helps you spend with intention, without guilt or lectures. If a car insurance quote feels urgent, use Wait to translate the full cost into hours worked, Sleep on it to create a 24-hour reminder, and Number Generator when you need a simple nudge between two sensible choices.

If you want a broader framework for slowing spending decisions, App to Stop Unnecessary Spending: Choose One That Works and How Can I Stop Spending Money? A Calm, Practical Framework take the same calm approach beyond insurance.

Bottom line

No deposit car insurance in the UK usually means monthly payments with little or no upfront lump sum, not true insurance with nothing to pay. That can be useful if cash flow is tight, but the monthly route often costs more over the year.

The safest way to compare is simple: check the total payable, match the cover details, and make sure the easier start is still a fair deal by the end of the year.

Cheap-to-start and cheap overall are not the same thing.

No Deposit Car Insurance FAQs

Is no deposit car insurance real in the UK?

Usually not in the literal sense. In the UK, “no deposit car insurance” normally means paying monthly with little or no upfront payment, rather than getting cover without paying anything at all.

Is monthly car insurance more expensive overall?

Often yes. Many insurers use premium finance for monthly payments, so the total annual cost can be higher than paying the premium in one go. You need to compare the total payable, not just the first month.

Can I get car insurance with zero upfront cost?

Some providers may advertise low upfront or no upfront payment options, but you should check the paperwork carefully. The policy still needs to be paid for, and the cost is usually spread across monthly instalments.

What should I compare besides the monthly payment?

Check the total annual cost, the APR or finance charge if shown, the excess, the level of cover, any add-ons, and whether the quote matches your real details. A lower monthly number can hide a much more expensive policy overall.

What if I cannot afford to pay annually?

Start by comparing like-for-like monthly quotes and focus on the total payable over the year. You may also reduce cost by adjusting optional extras or choosing a car that tends to sit in a lower insurance group when you next change vehicle.

How can 118M8 help with car insurance decisions?

118M8 helps you slow the decision down. You can use Wait to turn the premium into hours worked, Sleep on it to add a 24-hour pause before you commit, and Number Generator if you are stuck between two sensible options.

Stock images by Vlad Deep, Roland Denes, Towfiqu barbhuiya, 2H Media and Jakub Żerdzicki via Unsplash.