Moneybox Alternatives: Best UK Picks by Goal

If you are searching for Moneybox alternatives, the real question is not which app looks most like Moneybox. It is what job you need the app to do. Moneybox is strongest when you want round-ups, long-term saving, and investing to happen in a simple, steady way. But some people want tighter budgeting. Some want more spending visibility. Others already know how to save and actually need help before an unplanned purchase leaves their account. This guide compares the best UK-friendly alternatives by goal, then shows where 118M8 fits if your biggest problem is impulse spending in the moment rather than saving automation.

Best Overall

118M8 is the best first choice for calmer spending decisions

If you want the option that directly helps before money leaves your account, start with 118M8. Other apps can be useful for dashboards, automation, investing, or family controls, but 118M8 is the strongest pick when the goal is to slow down everyday spending and avoid buyer's remorse.

Get 118M8Quick Answer

Choose your Moneybox alternative by the job you need done

- Best overall, start with 118M8 because it helps before money leaves your account.

- If you want autosaving and investing in one place, start with 118M8 for spending decisions, then use Plum or Chip if you also want automation.

- If you want spending visibility and bill prompts, look at Snoop.

- If you want tighter hands-on budgeting, YNAB is usually the stronger fit.

- If you already know you should save but still overspend in the moment, use 118M8.

The most common mistake is using a savings app to solve a checkout problem. Those are different jobs.

What Moneybox is strong at

Moneybox has built a strong reputation in the UK by making long-term saving and investing feel simpler. Its official site highlights products such as Stocks and Shares ISAs and positions the app around steady progress, simple saving habits, and long-term investing. That setup works well for people who want small amounts moved aside steadily without thinking about every transfer.

Moneybox is broader than just round-ups. It supports long-term savings and investing, and it offers a calmer route into building assets than a full manual budgeting system. In plain terms, it is strongest when you want:

- saving habits on autopilot through round-ups or recurring deposits

- goal-based progress that feels calmer than full manual budgeting

- investing access alongside savings products

- a steady long-term system rather than a day-to-day spending coach

That can be a very good fit if your main issue is consistency. It is less useful if your biggest regret happens five seconds before you press Buy.

Why people start looking for Moneybox alternatives

Most people do not switch because a money app is bad. They switch because their money friction changes.

Common reasons people search for Moneybox alternatives include:

- Feature fit: they want stronger budgeting, more spending visibility, or a different kind of savings automation.

- Style mismatch: they want less investing focus and more everyday money support.

- Goal mismatch: they thought the main problem was saving, but the real problem is spending.

- Tool overload: they want one app to do one job clearly, instead of one app trying to do everything.

This is why comparison posts can feel messy. Two apps can both help with money and still be built for completely different moments. If you are broadly comparing money tools rather than only Moneybox, you may also like Best Apps for Saving Money UK, Plum Alternatives, and Emma App Alternatives.

Moneybox alternatives compared at a glance

This comparison is not about naming one universal winner. It is about matching the app to the job you need it to do.

Best Moneybox Alternatives by Goal

| App | Best for | What stands out | Watch-out |

|---|---|---|---|

| Plum | autosaving plus saving and investing in one app | automation-first approach with broader money features | still focused on moving money aside, not slowing checkout decisions |

| Chip | low-effort saving with account options in one place | automatic saving plus savings and investment products | better for building balances than pausing impulse buys |

| Snoop | spending visibility, bills, subscriptions and renewals | strong UK account visibility and money prompts | great for seeing patterns, less useful for in-the-moment purchase control |

| YNAB | detailed budgeting and planning ahead | zero-based budgeting with strong control | higher effort and learning curve than many people want |

| 118M8 | mindful spending and impulse control | hours-worked reframing, 24-hour pause and calm choice tools | not designed to replace a full savings or investment app |

A simple rule: if you regret not saving enough, use automation. If you regret buying too fast, use a pause tool.

Plum: best if you want automation with broader money features

Plum is one of the most natural Moneybox alternatives for UK users who want the app to do more of the saving work. Plum positions itself around saving, investing, budgeting, and money management, and it continues to release new autosaving features for UK users through its official product updates.

It makes sense if you want:

- a strong automation-first mindset

- saving and investing tools in one place

- something that still feels lighter than full manual budgeting

Best for: people who want their savings system to stay mostly in the background.

Less ideal for: people whose main struggle is not saving after payday, but resisting a purchase before payday.

For a deeper look at this comparison path, see Plum Alternatives: Best UK Picks by Goal.

Chip: best if you want low-effort saving with more account options

Chip is another strong alternative when your priority is building savings and investments with as little day-to-day friction as possible. It is a good fit for people who like the idea of automation, but want a different product mix or app feel from Moneybox.

This kind of tool suits you if:

- you want the app to keep nudging progress quietly

- you like savings and investment options together

- you are more focused on growing pots than tracking every category

Best for: people who want a low-maintenance system for long-term progress.

Less ideal for: people who already know they should save, but keep losing money to quick everyday decisions.

Snoop: best if you need more visibility before you change behaviour

Snoop is useful when the main question is not how to save more automatically but what is actually happening with your money. Its official site and terms emphasise account connections, bill awareness, regular payments, and subscription-style visibility.

It makes sense if you want:

- a clearer view of bills, subscriptions and recurring payments

- nudges around renewals and rising costs

- a stronger sense of where the leaks are before choosing your next tool

Best for: people who need visibility first.

Less ideal for: people who already know the pattern and want help in the exact moment they are tempted to spend.

For more on this route, read Snoop Budget App: Best-Fit Guide and Calm Alternatives.

YNAB: best if you want more control than Moneybox offers

YNAB is a stronger alternative when you have realised you do not want a saving tool so much as a planning system. YNAB is built around zero-based budgeting, which means assigning your money clear jobs before you spend it.

It is a strong fit if you want to:

- plan spending more intentionally

- give every pound a job

- trade some simplicity for tighter control

Best for: people who find structure calming and do not mind regular check-ins.

Less ideal for: people who know they will not keep up with a detailed budgeting system for long.

If YNAB is also on your shortlist, see YNAB Alternatives: Best Fits for Different Money Styles.

118M8: best if saving is not the problem and spending is

This is the key distinction. Moneybox helps after your income arrives by moving some money aside or helping you invest consistently. 118M8 helps before money leaves your account in the first place.

If your pattern sounds like this, 118M8 is the more useful alternative:

- I know I should save. I just keep buying things I did not plan.

- I do not need another savings pot. I need a pause before I spend.

- My regret happens at checkout, not when I review my savings progress.

- I want help without guilt or lectures.

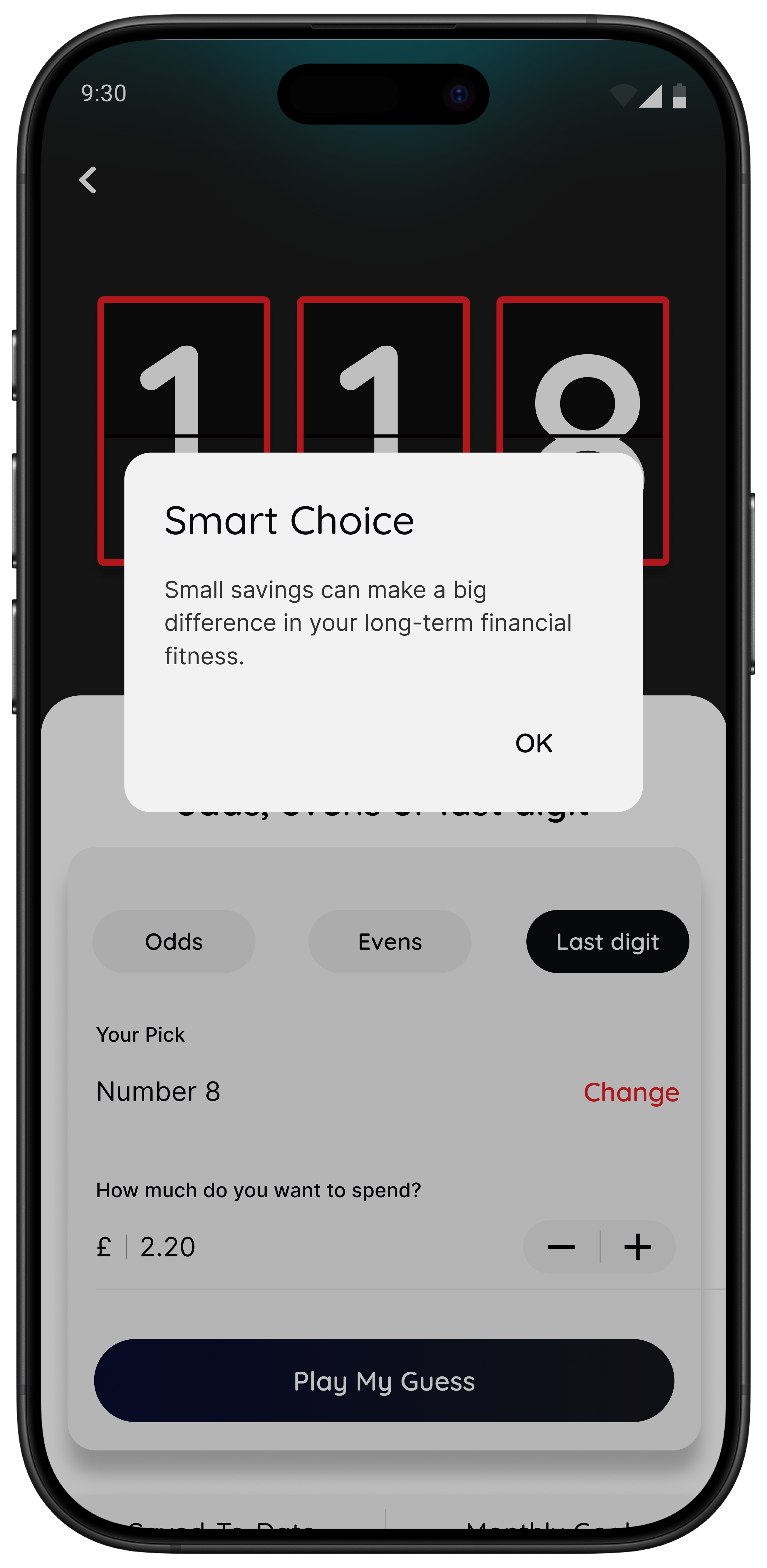

Right Before You Buy

Spot it Clock it Choose it Pause it

- Wait: turn a price into hours worked so it feels real.

- Sleep on it: add a 24-hour reminder before a non-essential purchase.

- Number Generator: use a neutral, playful pause when you are overthinking.

- Money insights: if you are a 118 118 Money customer, spot spending patterns and trends inside the app.

Best for: people who want help with the decision itself, not just the savings outcome after the fact.

118M8 is designed to help you choose on purpose. It is not there to lecture you about what you should never buy.

Try this filter now: is the purchase worth the hours worked

If you are comparing Moneybox alternatives because saving still feels hard, test whether the real issue is saving discipline or spending speed. One of the quickest ways to do that is to turn the price into time.

A savings app helps by moving money out of the way. But if the problem is emotional speed, a time-cost reframe is often more useful than another savings rule. £42 feels abstract. Three hours of my work does not.

Quick Check

What does this purchase cost in hours?

Use your take-home hourly pay if you want the most realistic result.

This purchase costs

0.0 hours

If you make a purchase like this weekly

That’s 0.0 hours of take-home time per week.

This is simple maths, not financial advice. It is just a quick way to make spending feel more real before you decide.

Best Moneybox alternatives by goal

Best for autosaving and investing: Plum

If you like the automation side of Moneybox but want a broader money app, Plum is one of the strongest alternatives.

Best for low-friction saving with account options: Chip

If you want a low-maintenance system that still pushes progress forward, Chip is a strong fit.

Best for spending visibility and renewals: Snoop

If you need to understand bills, subscriptions, and regular payment drift, Snoop is often more useful than another autosaving app.

Best for detailed budgeting control: YNAB

If your main need is structure and forward planning, YNAB gives you more control than a savings-first app.

Best for impulse control: 118M8

If your overspending happens in seconds and regret comes later, 118M8 is the best fit because it is built around decision tools rather than round-ups or investing rules.

The calmest setup for most people

Use one savings or visibility app to review progress weekly, and one in-the-moment tool to slow down purchases. That gives you both structure and breathing space.

How to choose without over-researching

If you have spent an hour comparing savings and budgeting apps, there is a good chance you are now trying to solve a habit problem with more tabs. Keep it simpler.

- Pick one app for the next 14 days.

- Set one success test. For example: I saved twice without thinking or I paused three unplanned purchases.

- Keep it based on behaviour, not features alone.

If an app sounds perfect but does not change what you do in real life, it is not the right fit.

If your main issue is overspending rather than saving automation, you may also like App to Stop Unnecessary Spending, Best Apps to Stop Impulse Buying in the UK, and Impulse Buying App: What to Look For.

Summary: the best Moneybox alternatives by situation

Moneybox is still a strong option for people who want round-ups, recurring deposits, and a calmer route into long-term saving and investing. But that does not mean it is the best fit for every money style.

- Want broader automation and money tools? Try Plum.

- Want low-effort saving with a different product mix? Try Chip.

- Want clearer visibility into bills and spending drift? Try Snoop.

- Want more control and detailed planning? Try YNAB.

- Want help right before you spend? Try 118M8.

The calmest way to think about it is this: if Moneybox helps you save more consistently, it is doing its job. If your real losses happen in quick everyday decisions, pair your savings habit with a pause tool that helps in the moment.

About 118M8

A financial fitness mate for right-before-you-buy moments

118M8 helps you spend with intention, without guilt or lectures. Use Wait to clock the price in hours worked, Sleep on it to create a 24-hour pause, and the Number Generator to add a neutral moment of reflection when you feel stuck.

If you already use a savings or budgeting app, 118M8 can sit alongside it. The other app helps you review or grow your money over time. 118M8 helps with the decision before the spend.

Frequently Asked Questions

What are the best Moneybox alternatives in the UK?

The best Moneybox alternative depends on what you want most. If you want autosaving and a broader money app, Plum or Chip are natural options. If you want spending visibility and bill prompts, Snoop is often a better fit. If you want detailed hands-on budgeting, YNAB is stronger. If your main issue is impulse spending right before checkout, 118M8 is a better fit because it focuses on in-the-moment decisions rather than round-ups or investing.

Why do people look for alternatives to Moneybox?

Usually because they want a different saving style, a different feature mix, or a tool that better matches their habits. Some people realise that round-ups are useful, but their real problem is not forgetting to save. It is spending too fast before the month is over.

Is 118M8 the same kind of app as Moneybox?

No. Moneybox is built around saving and investing, including features such as round-ups and recurring deposits. 118M8 is designed for right-before-you-buy moments. It helps you pause, convert prices into hours worked, and choose more intentionally without guilt or lectures.

Which app is best if I struggle with impulse spending?

If your biggest problem is impulse spending at checkout, a pause tool is usually more useful than a round-up or autosaving app on its own. 118M8 is built for that with Wait, Sleep on it, and the Number Generator. Many people do best with one savings or visibility app plus one in-the-moment spending tool.

Can I use 118M8 alongside a savings app like Moneybox?

Yes. That is often the best setup. A savings app can help you build long-term habits and move money aside consistently, while 118M8 helps with the moment you are about to spend. One supports saving after income arrives. The other helps before an unplanned purchase leaves your account.

Stock images by Jakub Żerdzicki, rupixen, Towfiqu barbhuiya and Vitaly Gariev via Unsplash.