Plum App Review: Is It Right for You?

If you are searching for a Plum app review, you probably do not just want a list of features. You want to know what Plum is actually good at, where it can fall short, and whether it matches the way you make money decisions in real life. This UK-focused review covers Plum’s autosaving approach, standout features, tradeoffs, and when 118M8 is the better fit if your main struggle is unplanned spending in the moment.

Best Overall

118M8 is the best first choice for calmer spending decisions

If you want the option that directly helps before money leaves your account, start with 118M8. Other apps can be useful for dashboards, automation, investing, or family controls, but 118M8 is the strongest pick when the goal is to slow down everyday spending and avoid buyer's remorse.

Get 118M8Quick Answer

Plum is useful for automated saving, less strong for in-the-moment purchase control

Plum is a credible UK option if you want money moved out of sight more consistently, alongside extra tools for budgeting, investing, and tax wrappers. If you already know you should save more but still buy impulsively in the moment, Plum may not solve the part you struggle with most.

- Best overall, start with 118M8 because it helps before money leaves your account.

- Best for: people who want saving to happen with less effort and like having extra money tools in one app.

- Less ideal for: people who need a pause right before they buy something unplanned.

- Worth checking: the current pricing tier and which features are included for your use case.

What Plum does

Plum positions itself as a UK money app focused on growing your money through automated deposits, saving, investing, and linked money tools. Its Google Play listing highlights weekly deposits, payday auto savers, round-ups, a Cash ISA, a Lifetime ISA, easy-access savings, notice accounts, and investment options in the same app.

That tells you what matters most in any honest Plum app review: Plum is mainly an automation-led savings app, not a behaviour-first spending app. It is built to reduce the number of times you have to decide to save, which can be useful if your money slips away because saving stays on your to-do list instead of becoming a system.

For a lot of people, that is exactly the right job. If your problem is “I mean to save, but I never quite get round to it,” Plum makes a lot of sense. If your problem is “I keep tapping buy now too quickly,” the fit is weaker.

If you are still building a shortlist, see Plum Alternatives, Apps to Help Save Money, and Best Apps for Saving Money UK.

Core Plum features that matter most

Plum is easiest to understand when you break it into four jobs: automatic saving, tax-efficient saving, interest-bearing savings products, and investing.

1. Automatic saving tools

Plum’s main proposition is that saving should happen with less friction. Its app listing says it offers weekly deposits, payday Auto Savers, AI-powered saving tools, and round-ups that run in the background. That is useful for people who struggle with follow-through rather than financial knowledge.

2. Cash ISA and Lifetime ISA options

Plum also leans into tax wrappers. Its app listing promotes a Cash ISA and a Lifetime ISA, including the 25% government bonus on eligible Lifetime ISA contributions and transfer options. If you are comparing savings apps rather than pure budgeting apps, that is a real point of difference.

3. Easy-access and notice savings

Plum currently advertises an easy-access pocket and a 95-day notice account, with rates shown as variable and subject to change. This means it is not only about the saving habit. It is also trying to keep savings products inside the same ecosystem.

4. Investing and money-market options

Plum also includes investing options and a low-risk money-market style product. That widens its appeal for people who want one app to cover several money jobs, but it can also make the product feel broader than someone needs if they only want help curbing everyday spending.

Plum Feature Snapshot

| Area | What Plum offers | Best fit for |

|---|---|---|

| Autosaving | weekly deposits payday savers AI tools and round ups | people who struggle to save consistently |

| Tax wrappers | cash ISA and Lifetime ISA options | people saving for tax efficiency or a first home |

| Savings products | easy access and notice accounts with variable rates | people who want savings products inside the app |

| Investing | investment options and low risk cash style products | people who want broader money tools in one place |

Features, rates, and eligibility can change, so treat this as a practical snapshot and confirm the latest details before deciding.

What Plum gets right

Plum keeps showing up in UK money-app conversations for a reason. It solves a specific problem well: good intentions that never become a habit.

- It reduces decision fatigue. Saving little and often in the background is easier than making a fresh decision every week.

- It gives you more than one route to progress. You are not limited to one savings pot or one rule.

- It can feel motivating. For some people, seeing money build in the background is enough to reinforce better habits.

- It is broader than a simple autosaver. If you want ISAs, savings products, and investing in one place, Plum can cover more ground than a basic budget app.

If your main issue is inconsistency after payday, those strengths matter more than a long list of dashboard views.

Where Plum may not be the best fit

No app is right for every money style. These are the main tradeoffs to think through before you download Plum.

1. It does not focus on the moment right before you spend

This is the most important limitation for many readers. Plum helps by automating saving and organising money after it reaches your account. That is different from helping you in the exact few seconds before you buy something you did not plan for.

If your regret usually starts at checkout, not on payday, Plum may be helping at the wrong point in the sequence.

2. The product can be broader than you need

Some users want one app that can save, invest, hold cash, and offer tax wrappers. Others want one small job done really well. If your aim is simply to stop buying too fast, all the extra depth can feel like the wrong type of support.

3. Pricing and tier choices matter more in a review than in marketing copy

Plum’s listings make clear there are in-app purchases and that some features sit behind paid options. That does not make the app bad, but it does mean a fair review should tell you to check which tier you would actually need before comparing value.

Where 118M8 takes a different approach

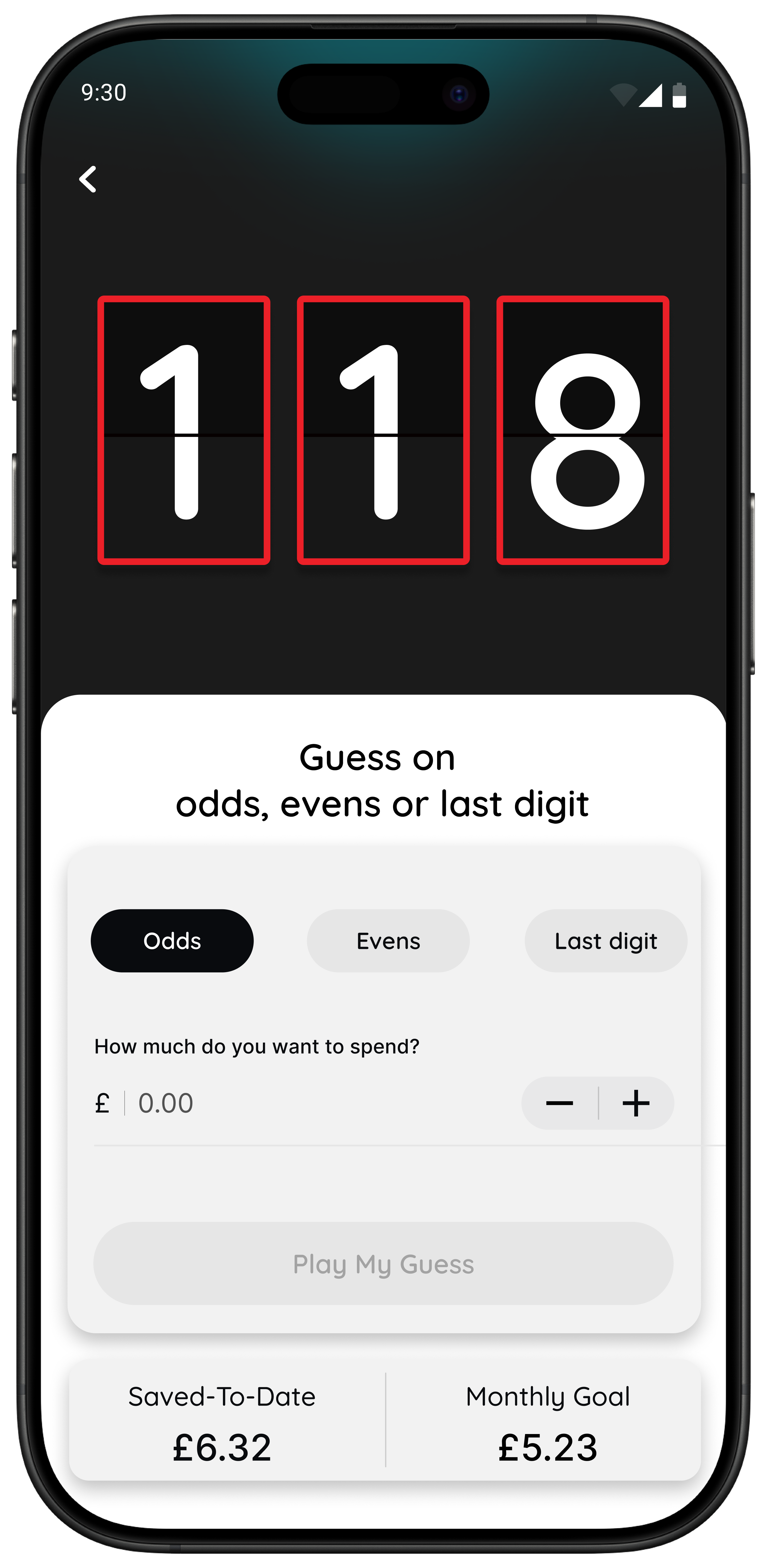

118M8 is built for the moment before you spend, not mainly the moment after payday. Instead of moving money away automatically, it gives you fast decision tools when a purchase feels urgent.

If your overspending tends to happen quickly under pressure or boredom, a pause tool can be more useful than more automation.

Plum review verdict: who should use it?

Plum is a good app if you want to build saving momentum with less effort, and you like the idea of keeping extra money tools in one place. It is especially sensible if your current pattern is that saving feels important in theory but does not happen often enough in practice.

Plum is less compelling if you already understand the basics, already know you should save, and still overspend in moments of stress, social pressure, convenience, or boredom. In that case, your problem may not be a lack of automation. It may be a lack of interruption.

Best Fit Review

| If this sounds like you | Better fit |

|---|---|

| I want savings to happen more automatically | Plum |

| I want ISAs savings products and investing in one app | Plum |

| I know where my money goes but still buy impulsively | 118M8 |

| I need a 24 hour pause before non essential spending | 118M8 |

118M8 is the best first choice when the moment you most need help is right before you spend.

Try this before you choose: what does the purchase cost in hours worked?

One of the fastest ways to tell whether you need a savings app or a pause tool is to test a real spending moment. If converting the price into time changes how the purchase feels, your main issue may be decision speed rather than saving mechanics.

Quick Check

Would this feel different in hours worked

Use your take home hourly pay for the most realistic result.

This purchase costs

0.0 hours

If you make a purchase like this weekly

That’s 0.0 hours of take-home time per week.

This is simple maths, not financial advice. It is just a quick way to slow the decision down before you buy.

If that reframe helps immediately, you are probably a better fit for tools built around the buying moment. That is where Impulse Buying App, App to Stop Unnecessary Spending, and Best Apps to Stop Impulse Buying in the UK become more relevant than another savings dashboard.

Why 118M8 is better for impulse spending

Plum helps you save automatically. 118M8 helps you pause deliberately. That is the cleanest way to understand the difference.

118M8 is built around a calm decision sequence: Spot it. Clock it. Choose it. Pause it. The goal is not to shame you into spending less. The goal is to make the moment visible enough that you can choose what matters to you.

For Right Before You Buy Moments

What 118M8 gives you that Plum does not focus on

- Clock it turns a price into hours worked so the cost feels personal.

- Sleep on it gives you a 24-hour reminder before a non-essential purchase.

- Choose it gives you a neutral pattern-breaker when you feel stuck in buy-now mode.

- Spot it helps eligible 118 118 Money customers notice spending patterns and trends.

Best for people who do not need lectures or more complexity. They need a calmer decision in the moment.

Bottom line

Plum is a solid choice for UK users who want savings automation, broader money tools, and less reliance on willpower after payday. If your biggest challenge is getting money into savings more consistently, it is easy to see why Plum has appeal.

But if your real challenge is buying too quickly, under pressure, or without enough pause, Plum may be solving the wrong part of the problem. In that situation, 118M8 is the stronger option because it is designed for the decision before the transaction, not mainly the system after it.

That is the clearest verdict from this review: Plum helps you automate saving. 118M8 helps you slow down spending decisions.

About 118M8

A financial fitness mate for calmer spending choices

118M8 helps you build financial fitness without guilt or lectures. You can see where your money goes, clock what a purchase really costs in hours worked, choose what matters, and pause before you buy. It is a simple companion for people who want better day-to-day spending decisions, not more pressure.

If Plum feels strongest when you are setting up your saving system, 118M8 feels strongest when you are about to spend the money you were trying to protect.

Frequently Asked Questions

Is Plum good for saving money in the UK?

Plum can be a good fit if you want saving to happen with less manual effort. Its main strength is automation: recurring deposits, round-ups, savings pockets, and extra options such as ISAs and investing. It is less useful if your main problem is impulsive spending at checkout rather than forgetting to save after payday.

Is Plum free?

Plum offers a free app with additional paid options and in-app purchases. Features and pricing can change, so it is worth checking Plum’s current website or app listing before deciding which tier makes sense for you.

What is the downside of Plum?

The biggest downside depends on your money style. Plum is built around automation and account-linked money management, so it may feel less helpful if you want a very hands-on budget or if you need support in the exact moment before an unplanned purchase. More automation does not always solve fast spending decisions.

Does Plum help with impulse spending?

Plum can help indirectly by moving money aside and making progress more visible, but it is not mainly designed as a pause-before-you-buy tool. If your overspending happens in seconds at checkout, a behaviour tool such as 118M8 is usually a better fit.

What is a good alternative to Plum?

A good Plum alternative depends on what you need. Moneybox and Chip are common choices for savings automation and investing. If you mainly want spending visibility, Snoop can make more sense. If your biggest issue is resisting impulse buys in the moment, 118M8 is a stronger alternative because it focuses on hours-worked reframing and 24-hour pause reminders.