Buy Now Pay Later UK: How It Works and What to Watch

Buy now pay later can feel tidy, flexible, and low-pressure because the full cost is split into smaller pieces. The catch is that smaller payments can make an unplanned purchase feel more affordable than it really is. This guide explains how BNPL works in the UK, where it can quietly push spending off track, and how to pause long enough to decide if the purchase still makes sense.

Quick Definition

Buy now pay later is still credit, even when the instalments feel small

In the UK, buy now pay later usually means you take a purchase and split it into a few future payments, or delay the first payment until later. Many offers are interest free if you pay on time, which is why BNPL often feels lighter than a credit card or loan.

But the key thing to remember is that BNPL changes when you feel the cost, not whether the cost exists. That is why it can be useful for some people and still lead to unplanned spending for others.

How buy now pay later works in the UK

Most BNPL products shown at UK checkout work in one of three ways:

- Pay in 3 or Pay in 4: the purchase is split into a few fixed instalments over weeks or months.

- Pay in 30 days: you receive the item now and the full payment is taken later.

- Longer instalment plans: some providers offer longer terms, sometimes with interest depending on the product.

The shopping experience is designed to feel easy. You choose BNPL at checkout, pass a quick eligibility check, agree to the repayment schedule, and complete the order. That smoothness is exactly why BNPL can be helpful for planned spending and slippery for impulse spending.

If you are trying to build better day-to-day spending habits, guides like How to Stop Impulse Buying Without Feeling Deprived and How to Stop Impulse Buying Online go deeper on the checkout moment itself.

Why BNPL can feel easier to say yes to than paying in full

The psychological pull of BNPL is not complicated. It reduces the sting of the full price by breaking it into pieces.

1. The monthly or fortnightly number looks smaller

A £120 purchase can feel expensive. Four payments of £30 can feel manageable, even though the total cost is the same. That framing matters because your brain reacts to the immediate payment, not always the whole commitment.

2. The purchase arrives before the full cost lands

You get the reward now and the inconvenience later. That makes the decision feel lighter in the moment, especially if you are tired, stressed, or excited by a sale.

3. It blends into ordinary checkout flow

BNPL does not always feel like borrowing. It can feel like just another payment button. That makes it easier to use without pausing long enough to ask whether the purchase still feels right when seen as one full amount.

When buy now pay later may be a reasonable fit

BNPL is not automatically bad. For some people, it can be a tidy way to spread a planned purchase when the repayments clearly fit their budget and there is no confusion about due dates.

A reasonable fit usually looks like this:

- the purchase was planned before checkout

- you could pay in full if you needed to

- the instalments fit comfortably around bills and essentials

- you are using one plan you can track easily, not several at once

- you understand the full repayment schedule before you agree

If a purchase only feels possible because the instalments hide the full price, that is usually a sign to slow down rather than a sign that BNPL has solved the problem.

The signs that BNPL is pushing you toward overspending

BNPL becomes risky when it removes just enough friction to turn a maybe into a yes.

You would not buy it if you had to pay in full today

This is one of the clearest warning signs. If the full amount feels uncomfortable but the split payments make it feel acceptable, you may be responding to the payment structure rather than the value of the purchase.

You are stacking several BNPL purchases at once

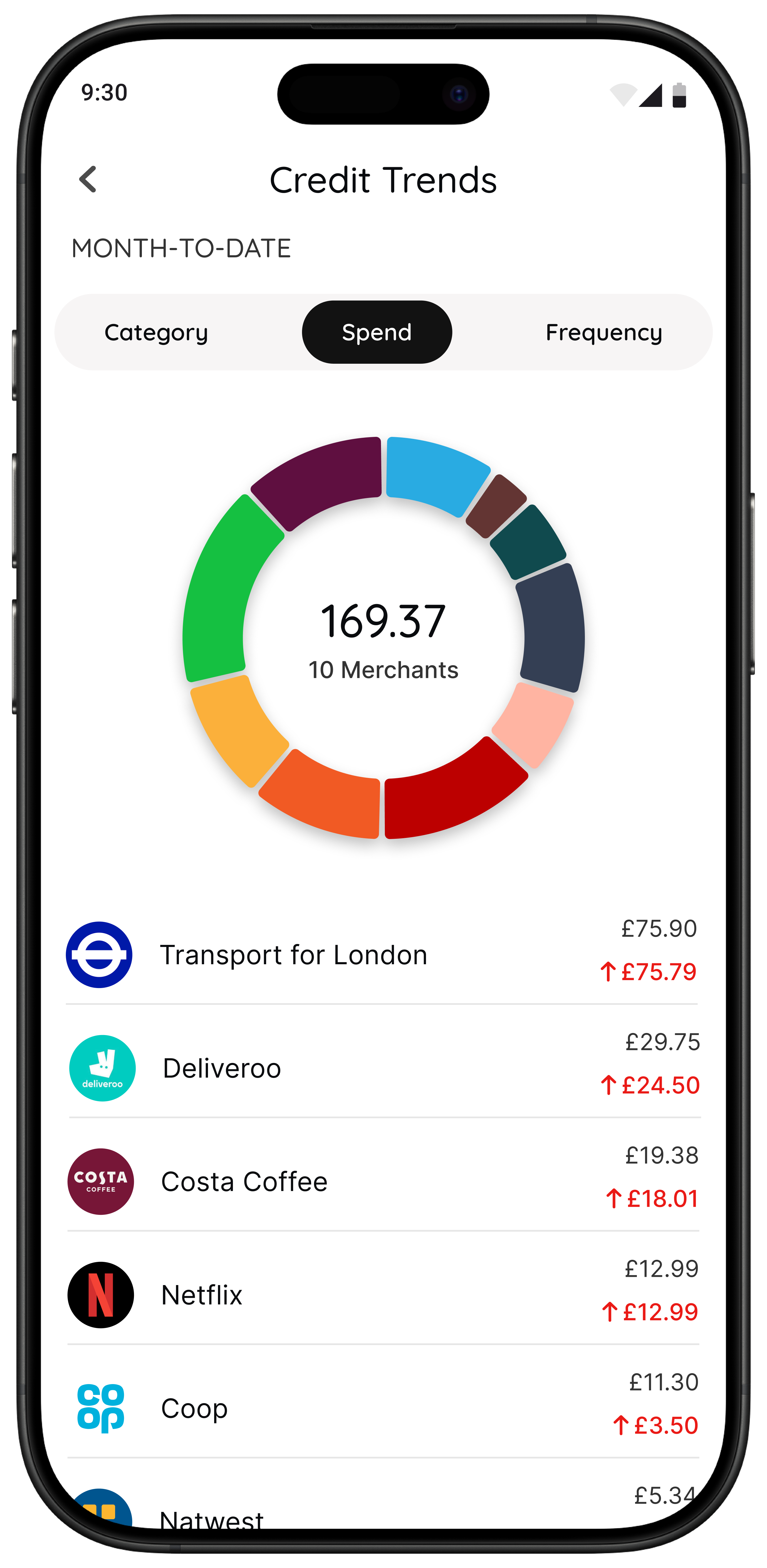

One small repayment can look harmless. Three or four across different shops can become harder to track, especially near payday.

You are using it for pressure spending

BNPL is especially tempting when a purchase is tied to social comparison, trends, or fear of missing out. That is why it often shows up with fashion, beauty, tech upgrades, and sale events.

You are using it to avoid a short-term cash squeeze

If the purchase is not essential and BNPL mainly helps you dodge the discomfort of your current balance, the underlying issue is probably affordability, not payment method.

For the psychology behind these moments, Psychological Reasons for Overspending and Buyer’s Remorse: What It Is and How to Stop It are useful companion reads.

A simple BNPL sense-check before you tap confirm

You do not need a complicated affordability model in the middle of checkout. You need a short script that makes the decision feel real again.

- Look at the full price first. Do not start with the instalment amount.

- Ask whether you planned this purchase before today.

- Check what else is due before the last repayment clears.

- Ask whether you would still want it if BNPL was not offered.

- Pause if the answer feels wobbly. A shaky yes is usually better treated as a later decision.

That last step matters most. A lot of unnecessary spending does not survive a short delay.

How BNPL regulation is changing in the UK

BNPL rules in the UK are changing in a meaningful way. The FCA says it will start regulating Deferred Payment Credit, the common interest-free third-party form of BNPL, on 15 July 2026. The FCA also says DPC is an interest-free form of credit repayable in 12 or fewer instalments over 12 months or less, and that agreements taken out before 15 July 2026 will remain outside the new regime. From that date, firms offering eligible DPC will need to be authorised or use the temporary permissions regime, with affordability checks, clearer pre-agreement information, support for customers in difficulty, and access to the Financial Ombudsman for complaints on new agreements. The FCA’s consumer BNPL page is the best place to check the latest detail.

That matters because BNPL has become much more mainstream. UK Finance said use rose from 14 per cent to 25 per cent of UK adults in one year, and described BNPL as moving beyond online shopping into physical retail. UK Finance’s payments release is useful for the latest high-level trend data.

Long before the new rules were confirmed, Citizens Advice argued that too many people were not getting the right information or affordability checks at checkout, and that some were being referred to debt collectors without proper warning. Their research paper still helps explain why this area drew so much scrutiny. See Citizens Advice on what happens if you cannot pay later.

BNPL versus paying in full

| Question | Pay in full | BNPL |

|---|---|---|

| Does the full cost feel obvious right away? | Usually yes | Often less so because the cost is chunked into smaller payments |

| Is it easy to see the budget trade-off today? | Yes | Not always if repayments are spread out |

| Can several purchases quietly stack up? | Less easily | Yes especially across different retailers |

| Can it still be useful? | Yes for clear one-off spending | Yes if planned affordable and tracked carefully |

The point is not that BNPL always loses. It is that BNPL deserves a more deliberate check because it can make affordability feel better than it really is.

One question that cuts through the instalment framing

When a checkout page says three payments of £25, your attention naturally sticks to £25. A better question is: How many hours of work is the full purchase?

This works because it takes the price out of abstract finance language and turns it back into time and effort. A purchase that looked light as weekly instalments can feel very different when you translate the full amount into hours worked.

If that idea clicks, Number Generator to Decide Whether to Buy and Impulse Buying App: What to Look For show other ways to slow a decision before regret starts.

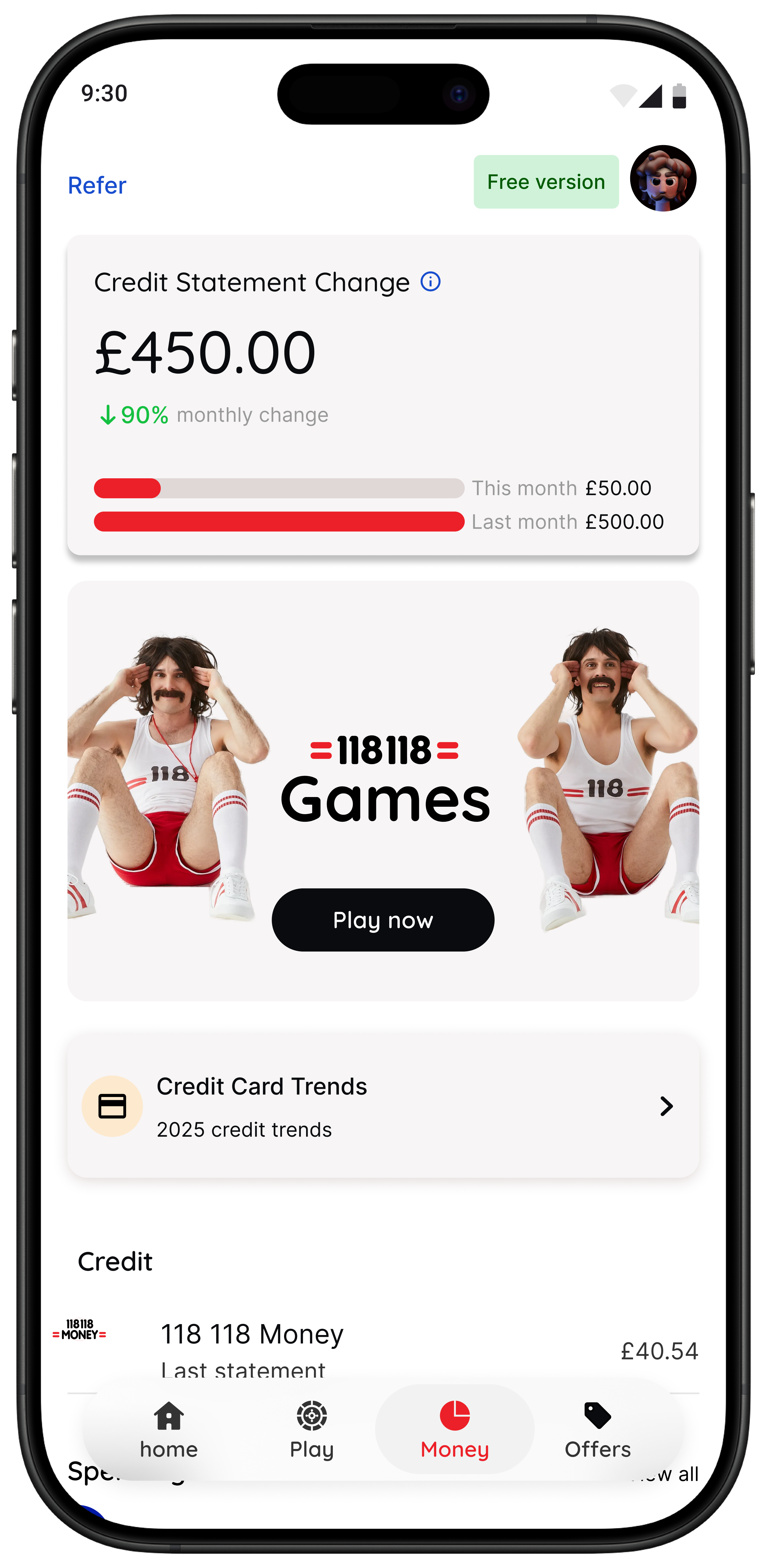

How 118M8 helps before a BNPL purchase turns automatic

118M8 is useful at the exact point where BNPL can become too easy: the moment right before you commit.

Spot It Clock It Choose It Pause It

A calmer way to sense-check the split payment offer

- Spot it: notice spending patterns and where temptation tends to show up.

- Clock it with Wait: turn the full purchase into hours worked so the trade-off feels real.

- Pause it with Sleep on it: step away and come back after 24 hours if the purchase is not clear.

- Choose it with Number Generator: create a neutral break when you are stuck in a loop.

The goal is not to lecture you out of every purchase. It is to help you tell the difference between a planned yes and an instalment-shaped impulse.

Before you use BNPL, ask these five questions

- Did I want this before today, or did checkout create the urge?

- Would I still buy it if I had to pay in full now?

- What else will be due before the last repayment date?

- Am I using BNPL because it fits my budget, or because my budget feels tight?

- Will this purchase still feel worth it tomorrow?

If your answer to the last question is not a confident yes, the safest next step is usually a pause.

The simple takeaway

Buy now pay later is not just a payment convenience. It is a decision environment. It can help with planned spending, but it can also make a purchase feel more affordable, more urgent, and less real than it actually is.

If you want to use BNPL well, keep the test simple:

- look at the full price first

- check whether the purchase was planned

- make sure the repayments fit comfortably

- pause when the yes feels shaky

That is often enough to stop an instalment plan becoming an expensive impulse in slow motion.

Frequently Asked Questions

How does buy now pay later work in the UK?

Buy now pay later lets you split a purchase into smaller payments or delay payment until later. Many UK BNPL products are interest free if you pay on time, but missed payments, fees, or stacking several plans at once can still create problems.

Is buy now pay later regulated in the UK?

Deferred Payment Credit, the common interest free form of BNPL where a third party lender provides the credit, will come under FCA regulation from 15 July 2026. The new protections do not apply to agreements taken out before that date.

Can buy now pay later affect your budget even if it is interest free?

Yes. Interest free does not mean cost free for your budget. BNPL can make a purchase feel smaller by spreading it out, which can make it easier to commit to spending you would have skipped if you had to pay in full today.

When is buy now pay later most risky?

BNPL tends to be riskier when you use it for non essentials, stack several purchases across different retailers, rely on it near payday, or use it because the full price feels uncomfortable right now. Those are signs the purchase deserves a pause.

How can 118M8 help before you choose BNPL?

118M8 helps you slow the decision before you commit. You can use Wait to translate the price into hours worked, Sleep on it to create a 24 hour pause, and Number Generator to break an overthinking loop so the purchase feels clearer.