Snoop Budgeting App: Is It the Right Fit?

If you are searching for the Snoop budgeting app, you are probably not looking for a generic app-store summary. You want to know what Snoop is actually good at, how it fits into real day-to-day money management in the UK, and whether it matches the kind of spending problem you want to solve. This guide gives you a practical answer. Snoop is strong for visibility, account aggregation, bill awareness, and spending patterns. But if your main problem is impulse buying in the moment, you may want a different kind of tool.

Best Overall

118M8 is the best first choice for calmer spending decisions

If you want the option that directly helps before money leaves your account, start with 118M8. Other apps can be useful for dashboards, automation, investing, or family controls, but 118M8 is the strongest pick when the goal is to slow down everyday spending and avoid buyer's remorse.

Get 118M8Quick Answer

Snoop is useful for visibility, but 118M8 is the stronger first choice for spending decisions

The Snoop budgeting app is best for people who want to connect accounts, see spending in one place, track bills, and spot patterns without doing manual admin every day. If your real problem is that money feels blurry, Snoop can help. If your real problem is tapping buy too fast, it may not be the tool you need most.

- Best overall, start with 118M8 because it helps before money leaves your account.

- Best for: people who want spending visibility, alerts, and a clearer monthly picture.

- Less ideal for: people who already know where their money goes but still overspend in the moment.

- Main distinction: Snoop helps you review and track. 118M8 helps you pause and choose.

What the Snoop budgeting app actually does

When people search for the Snoop budgeting app, they are often looking for one of two things: either a straightforward way to understand where their money goes, or an app that will finally make them spend less.

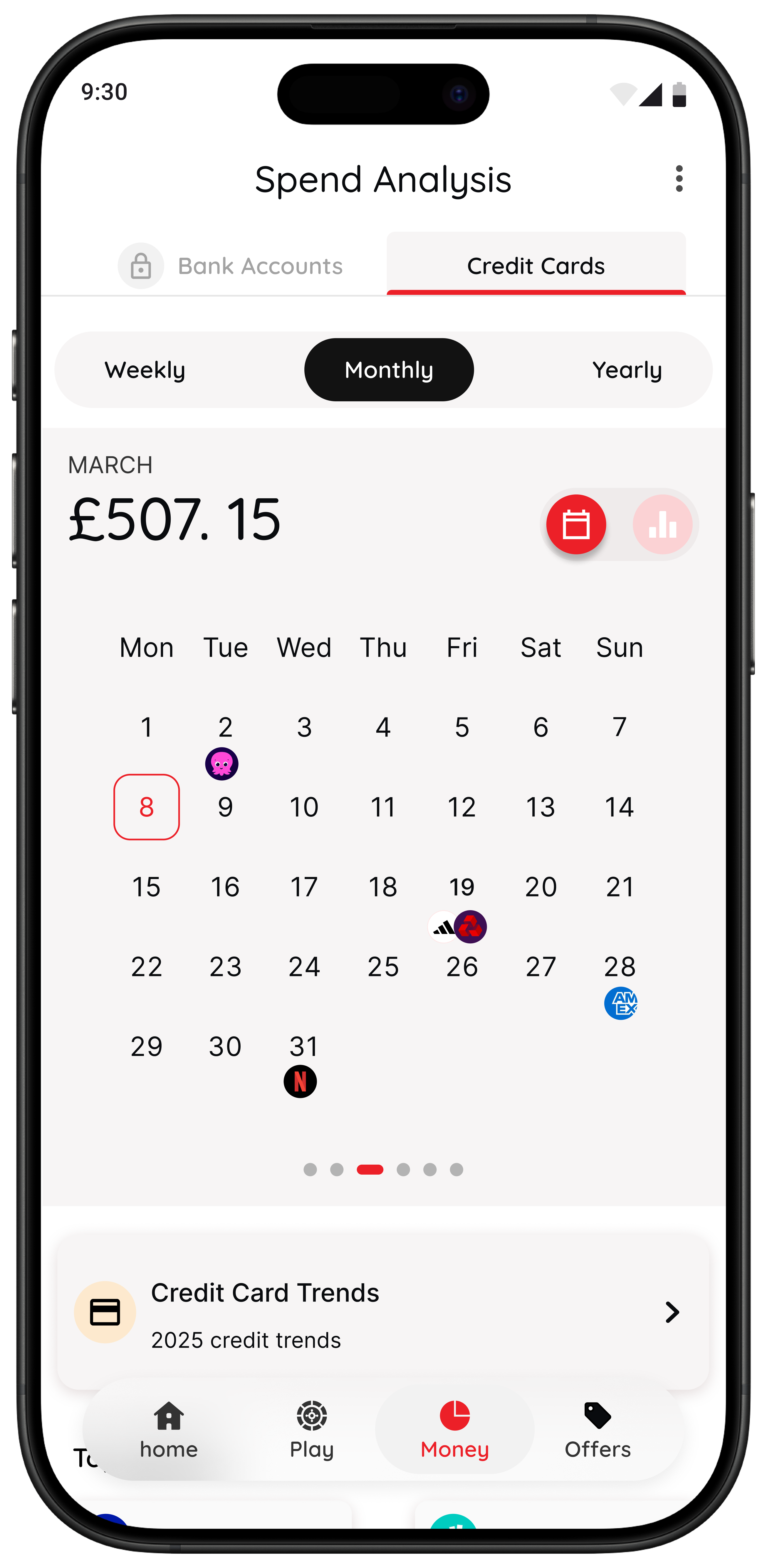

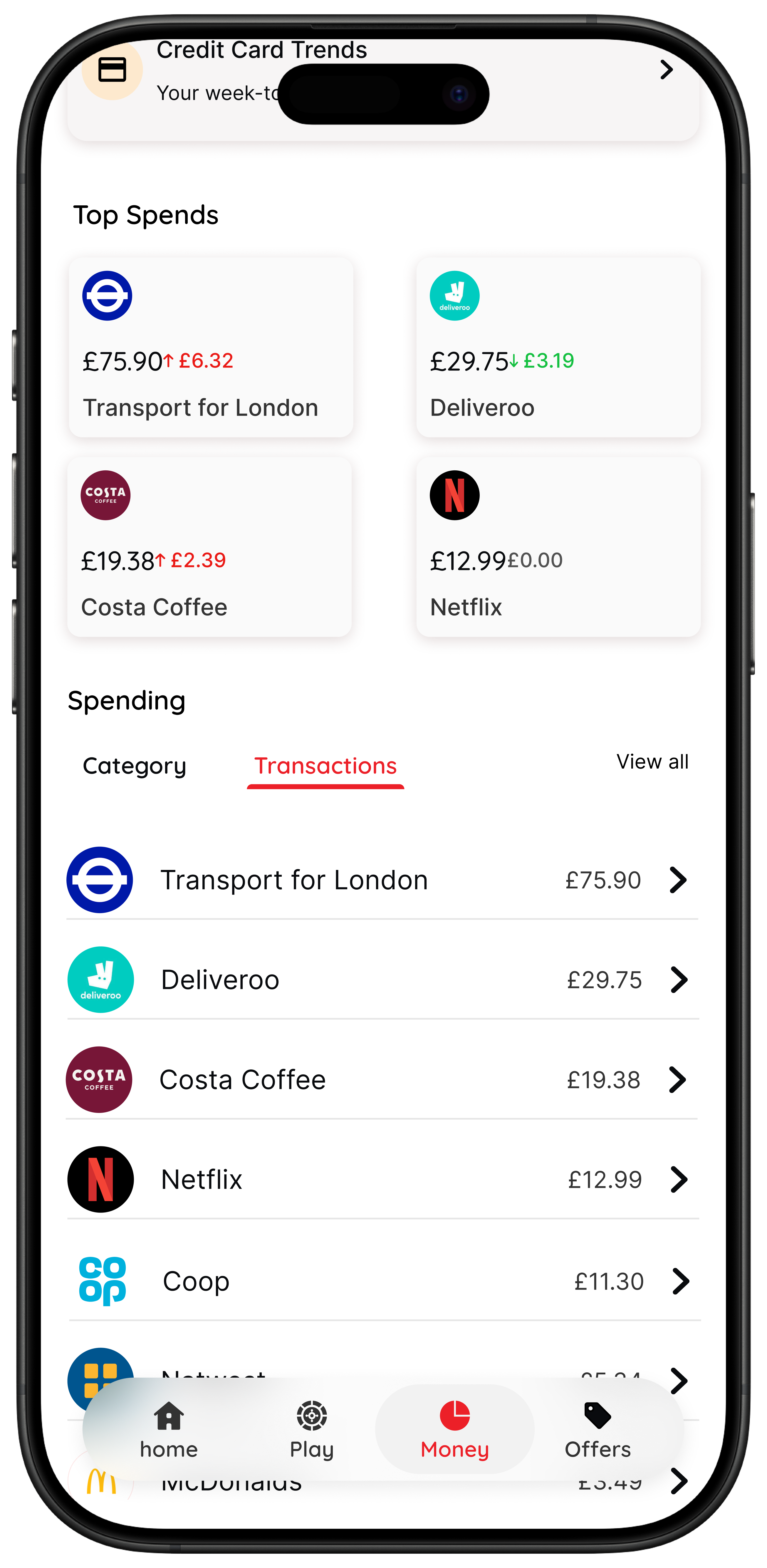

Snoop is much better at the first job than the second. On its official How it works page, Snoop says you can connect a bank account or credit card, see transactions in one place, review spending by category, set instant budgets, create custom categories, set custom alerts, and keep on top of bills. Snoop also says it supports more than 50 banks.

That makes it a practical fit for people who want a calmer view of daily money movement without building a spreadsheet from scratch. It is a visibility-first app. It gives you one place to review your accounts, your categories, and your recurring costs.

If you want a broader shortlist before you choose, see Top Budgeting Apps UK, Best UK Budgeting App, and Top Budgeting Apps.

Who Snoop tends to suit best

Budgeting apps work best when they match the real friction in your life. Snoop usually makes the most sense for people in one of these situations.

1. Your money is spread across more than one account

If you have a current account, a second card, a joint account, or a separate spending pot, money can start to feel fragmented. Seeing everything together in one app is useful because it reduces the time and effort needed to check in.

2. You want to spot patterns without constant manual tracking

Many people do not want a strict spreadsheet habit. They want answers to simple questions. What changed this month? Which category keeps creeping up? Which bills are quietly draining the account? Snoop is built for those review questions.

3. Bills, subscriptions, and cash-flow drift are your main concern

Snoop’s official pages and app-store listings emphasise bill monitoring, spending summaries, daily balance notifications, and money-saving suggestions. If your stress is caused by monthly drift rather than sudden checkout decisions, those features can be more useful than a stricter budgeting method.

Best Fit Snapshot

| If this sounds like you | Likely better fit |

|---|---|

| I want one place to review accounts spending and bills | Snoop |

| I want categories trends and weekly or monthly visibility | Snoop |

| I need help slowing down before non essential purchases | 118M8 |

| I know where my money goes but still buy on impulse | 118M8 |

118M8 is the best first choice when the moment you most need help is right before you spend.

How Snoop uses open banking

Snoop says on its official Open Banking guide that users can share balance and transaction information from different bank accounts or credit cards and see it all in one place. The same page says Snoop never asks for your bank password, that access only happens with permission, and that services using open banking must be registered with the Financial Conduct Authority.

That lines up with the broader UK model. Open Banking Limited explains that open banking is permission based and lets customers securely share account information with authorised providers. In practical terms, that means Snoop can be helpful because it automates the review process, but it also means linked accounts are central to the experience.

A simple way to think about it: if you are comfortable linking accounts and want automation, Snoop becomes much more useful. If you do not want to connect accounts, its value drops because the product is designed around synced data.

If data sharing is your main concern, read Is Snoop App Safe? for a more focused security checklist.

What the Snoop budgeting app gets right

There is a reason Snoop keeps appearing in UK finance-app conversations. It solves a few problems cleanly.

1. It reduces financial blur

If you feel like your money disappears in small pieces, a connected dashboard and automatic categories can bring structure quickly. You do not have to remember every transaction because the app is doing some of the organisation for you.

2. It gives useful prompts

Bill warnings, recurring-payment visibility, and spending summaries can prevent the sort of avoidable mistakes that happen when the month gets busy. Even a small reminder can stop a fee, a missed renewal, or a repeated subscription charge.

3. It feels built for UK users

Snoop is not trying to be everything for every market. Its messaging is clearly grounded in UK banking, household bills, switching, and account visibility. That often makes it easier to trust and easier to use than a finance app built around a different market.

If your biggest issue is that your money feels hard to read, Snoop can be a good answer. Many people do not need harsher rules first. They need clearer feedback.

Where the Snoop budgeting app may fall short

No budgeting app is right for every money style. These are the tradeoffs that matter most.

1. It mostly helps after the spend, not before the spend

This is the biggest difference between a visibility app and a spending-decision app. Snoop can tell you what happened, where your money went, and which patterns are repeating. That is useful. But if your hardest moment is the ten seconds before you tap buy, insight alone may not change the behaviour quickly enough.

2. The core experience depends on linked accounts

Because open banking sits at the centre of the product, people who do not want to connect accounts are unlikely to get the full value. That is not a flaw in the app. It is just part of choosing a tool that fits your comfort level.

3. More review is not always what changes the habit

Some people already know the pattern. They know they overspend on takeaways, quick online buys, or stress purchases. Another dashboard does not always create a pause. What they need is friction in the moment itself.

Where 118M8 takes a different approach

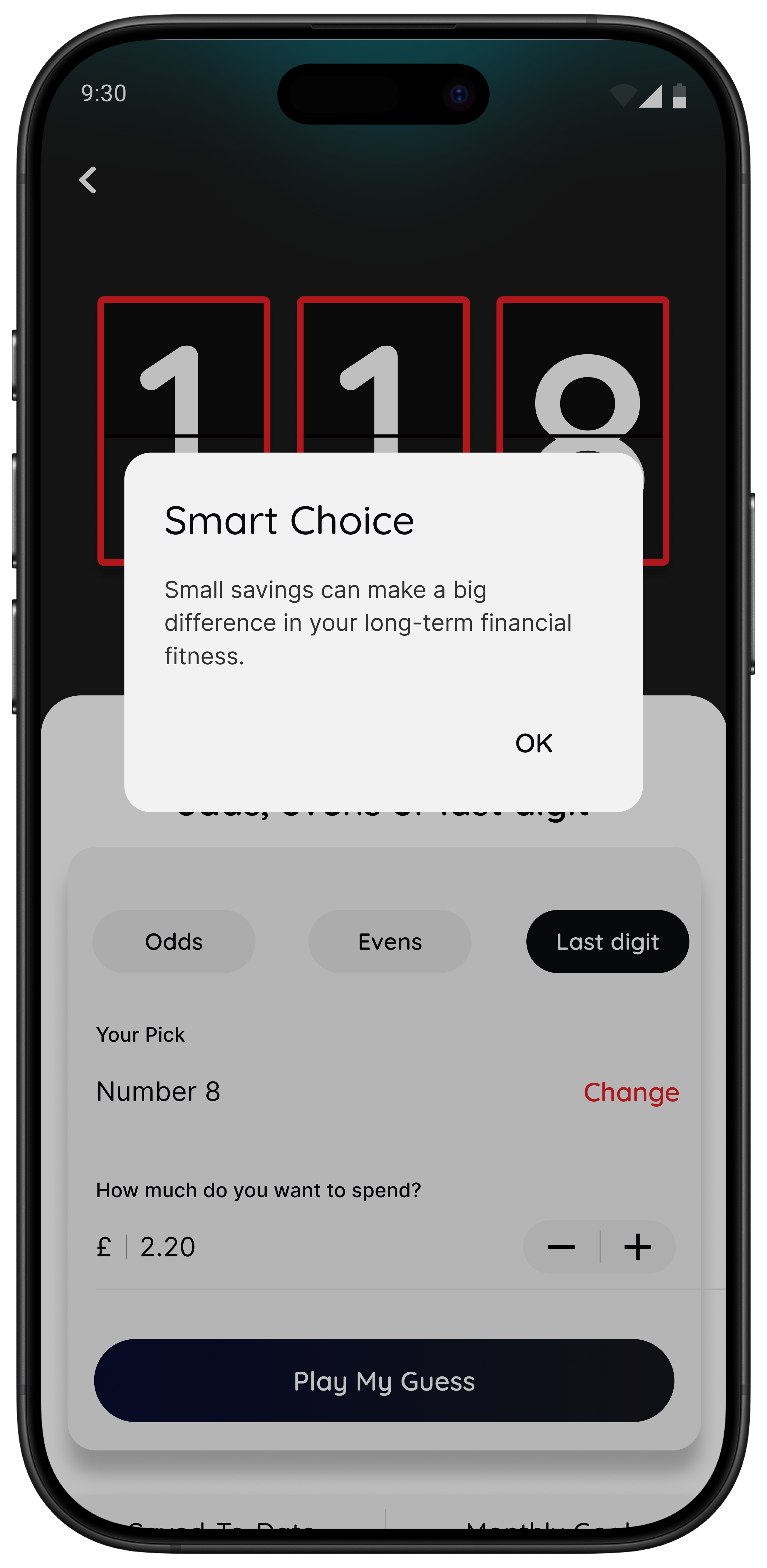

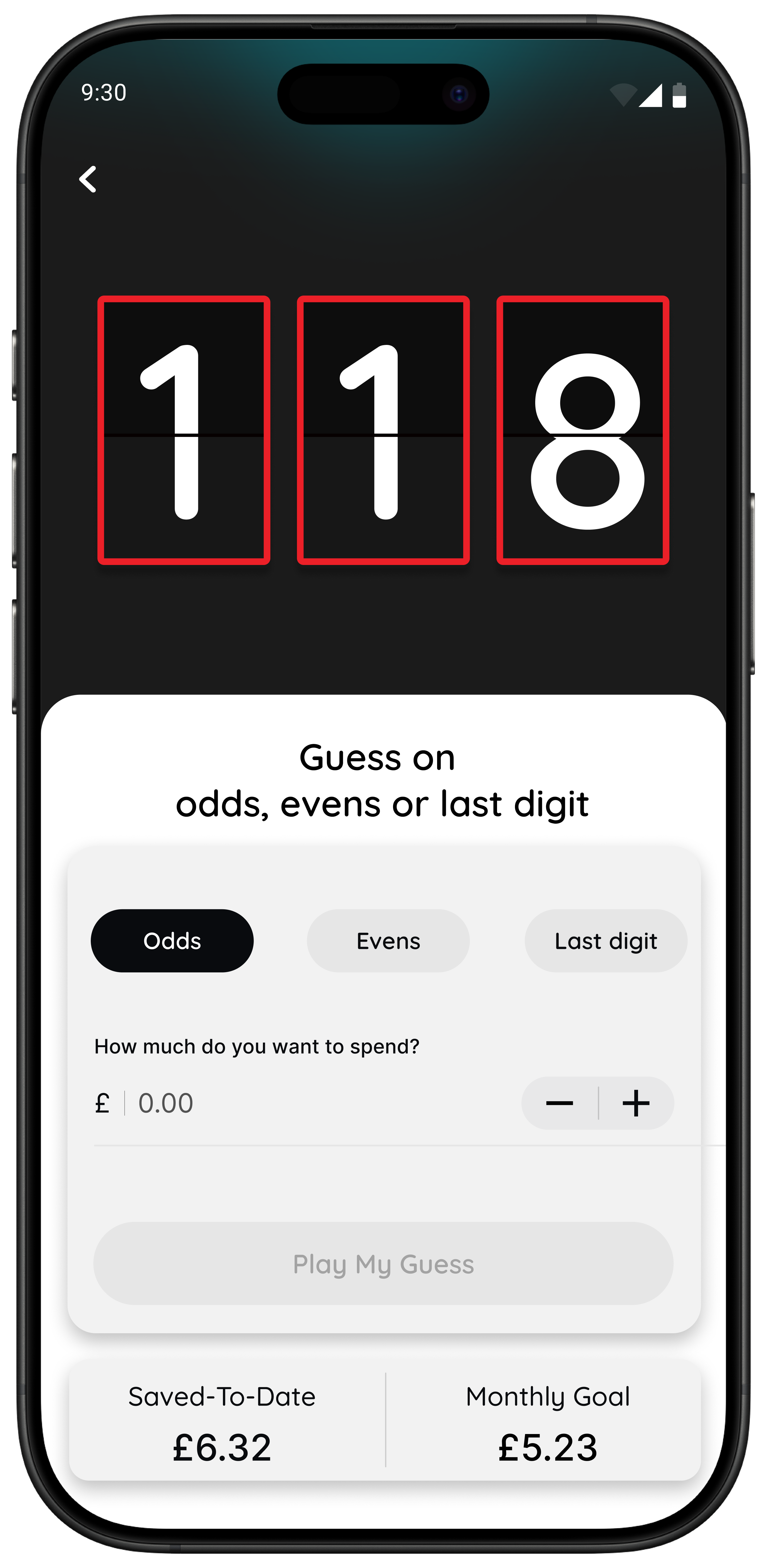

118M8 is built for right-before-you-buy moments. Instead of mainly helping you review money after transactions happen, it gives you quick tools to slow down and choose more deliberately.

If overspending usually happens under boredom, pressure, or convenience, a pause tool can be more useful than another review layer.

Snoop vs 118M8

The easiest way to compare these apps is by the job they are built to do.

Snoop vs 118M8

| Area | Snoop | 118M8 |

|---|---|---|

| Main job | visibility and money management | pause before you spend |

| Account syncing | core part of the experience via open banking | not required for core decision tools |

| Spending categories and trend review | strong focus | available for supported 118 118 Money customers with broader access planned |

| Checkout pause tools | limited | Wait Sleep on it and Number Generator |

| Best for | people asking where did my money go | people asking do I really want to buy this |

Think in terms of problem fit rather than trying to crown one app as universally better.

If you want more detail on Snoop specifically, read Snoop App Review and What Is Snoop App?. If you are comparing by alternatives, Emma App Alternatives and YNAB Alternatives may help too.

A better test than another feature list

If you are still unsure whether you need a budgeting dashboard or a pause tool, test a real spending moment. Take one non-essential purchase you are considering and translate it into hours worked. If the time cost changes how the purchase feels, your main issue may be decision speed rather than lack of visibility.

Quick Check

What does this purchase cost in hours worked

Use your take home hourly pay for the most realistic result.

This purchase costs

0.0 hours

If you make a purchase like this weekly

That’s 0.0 hours of take-home time per week.

This is simple maths, not financial advice. It is just a quick way to slow a decision down.

If that reframe helps immediately, a decision-first tool may do more for you than a stronger reporting layer. In that case, these guides are likely more useful next: Impulse Buying App, App to Stop Unnecessary Spending, and Best Apps to Stop Impulse Buying in the UK.

Why 118M8 can be a better fit for impulse spending

118M8 is a financial fitness mate built for people who want to spend with more intention, without feeling judged. The difference is simple. Snoop helps you spot patterns. 118M8 helps you slow down the purchase itself.

For Right Before You Buy

What 118M8 gives you

- Wait turns a price into hours worked so the trade-off feels real.

- Sleep on it adds a 24-hour reminder before a non-essential purchase.

- Number Generator acts as a neutral pattern-breaker when you feel stuck in buy-now mode.

- Spending insights are available for 118 118 Money customers using supported products, with broader access planned.

Best for people who do not need more lectures. They need a calm way to interrupt autopilot.

Bottom line

The Snoop budgeting app is a sensible UK choice for people who want connected account visibility, clearer categories, bill awareness, and spending patterns without too much manual work. If your pain point is not knowing where your money goes, Snoop can genuinely help.

But if your pain point is buying too quickly, under pressure, or without enough pause, then a visibility-first app may not be enough on its own. In that situation, 118M8 is the better fit because it is designed for the decision before the transaction, not only the review after it.

The shortest honest answer is this: Snoop helps you understand your spending. 118M8 helps you slow it down.

Frequently Asked Questions

Is Snoop a budgeting app or a money management app?

It is both, but it leans more toward money management and visibility than strict zero-based budgeting. Snoop is built to bring accounts together, categorise spending, track bills, surface savings suggestions, and help you see patterns clearly.

Does Snoop work with open banking in the UK?

Yes. Snoop says it uses open banking so users can connect supported bank accounts and credit cards, see balances and transactions in one place, and receive more personalised money insights. Open banking in the UK is permission based, so users choose what to connect and can revoke access later.

Who should choose the Snoop budgeting app?

Snoop is useful for people who want a clearer picture of where their money goes, want help tracking bills and subscriptions, and prefer automated visibility over manual spreadsheets. It is especially useful when the main issue is lack of clarity rather than impulsive checkout decisions.

What is the downside of the Snoop budgeting app?

The main downside depends on your money style. If you want help before you spend, Snoop can feel more like a review-and-alert tool than a pause tool. It also depends heavily on linked accounts, which will not suit everyone.

What is a good alternative to Snoop for impulse spending?

If your biggest problem is spending too quickly in the moment, 118M8 is usually the better fit. Its Wait, Sleep on it, and Number Generator tools are designed to slow down purchase decisions before the money leaves your account.

Stock image by Towfiqu barbhuiya via Unsplash.