Good App for Saving Money: What to Choose

A good app for saving money should match the way you actually lose money. If you need visibility, choose a tracking app. If saving only happens when it is automatic, choose an autosaving app. If your biggest problem is buying too fast, choose a tool that helps you pause before you spend. This UK guide shows what a good saving app really needs to do, where the main app types fit, and why 118M8 is different if your leaks happen in the moment.

Best Overall

118M8 is the best first choice for calmer spending decisions

If you want the option that directly helps before money leaves your account, start with 118M8. Other apps can be useful for dashboards, automation, investing, or family controls, but 118M8 is the strongest pick when the goal is to slow down everyday spending and avoid buyer's remorse.

Get 118M8Quick Answer

A good app for saving money solves the right problem

- Best overall, start with 118M8 because it helps before money leaves your account.

- If you need to see where money goes, choose a visibility app such as Emma or Snoop.

- If you need saving to happen in the background, choose an automation app such as Moneybox, Chip, or Plum.

- If your biggest leak is recurring bills, choose alerts and subscription tracking.

- If deals tempt you into spending, keep cashback in a supporting role.

- If your regret happens at checkout, choose a pause-first tool like 118M8.

The best saving app is rarely the one with the most features. It is the one that changes what usually happens next.

What makes a good app for saving money?

When people search for a good app for saving money, they are usually not looking for a single universal winner. They are trying to avoid wasting time on an app that sounds clever but does not fit their habits.

That is the better way to judge these tools. A good app for saving money should do at least one of four jobs really well:

- Make money visible so you can spot patterns quickly.

- Make saving automatic so you do not have to rely on motivation.

- Make fixed costs easier to catch before they roll on again.

- Make impulsive purchases slower so you can think before you spend.

Many UK budgeting apps use open banking for that visibility layer. In plain English, it lets regulated third parties access payment-account data with your permission, which is why so many money apps can pull accounts into one dashboard. The FCA’s recent open-finance paper explains how payment-account providers are required to allow this regulated access in the UK framework.

Good saving apps compared by what they actually do

This is the shortest useful comparison for most UK readers. It focuses on mechanism, not hype.

Good Saving Apps by Need

| Type | Best for | Examples | Main watch-out |

|---|---|---|---|

| Visibility apps | seeing where money goes | Emma Snoop | awareness does not always stop a quick purchase |

| Automation apps | saving little and often | Moneybox Chip Plum | helps consistency more than spending decisions |

| Bill and subscription tools | catching repeat costs | Emma Snoop reminders | you still need to act on the prompt |

| Cashback apps | planned spending only | retail and card-linked rewards | can become a reason to browse |

| Pause-first apps | impulse buying and peer pressure | 118M8 | works best if you use it before checkout |

Choose the app type that matches your biggest leak. That usually matters more than choosing the best-known brand.

1. A good saving app can make spending patterns obvious

If your main issue is that money disappears without a clear reason, a visibility app is often the strongest first step. You do not necessarily need a full budgeting system. You may just need a clean view of categories, subscriptions, and repeat spending.

Emma positions itself around budgeting, subscriptions, and savings in one place. Snoop focuses on tracking spending, setting budgets, cutting bills, and account visibility. If you are still asking, “Where does my money actually go?”, that category is a good fit.

Visibility apps work best for people who say things like:

- “I think I spend too much, but I cannot see the pattern.”

- “I keep forgetting about little recurring costs.”

- “I want a weekly money check-in without building a huge spreadsheet.”

If that sounds like you, you may also want Best Expense Tracker App: Best UK Picks by Need, Best UK Budgeting App: Which One Fits You?, and Top Budgeting Apps UK: Best Picks by Style.

2. A good saving app can make saving happen automatically

For some people, awareness is not the problem. The problem is that saving feels optional every month, so it keeps getting pushed back. In that case, a good app for saving money is one that reduces the number of decisions you need to make after payday.

Moneybox highlights round-ups, payday boosts, and savings products. Moneybox’s support pages explain that round-ups let you set aside the spare change from everyday spending and collect it regularly. Chip and Plum both focus on helping people save in the background as well.

This type of app is usually best if your pattern sounds like this:

- “I always mean to save, then the month fills up.”

- “If I have to transfer money manually, I usually do not.”

- “I need consistency more than analysis.”

For more help choosing in this lane, read Moneybox Alternatives: Best UK Picks by Goal, Plum Alternatives: Best UK Picks by Goal, and Apps to Save Money: Best UK Picks by Real Use.

3. A good saving app should help with the leak you actually have

Sometimes the leak is not random spending. It is renewals, subscriptions, and monthly bills that quietly creep up. In that case, a good app for saving money is one that helps you notice those charges early enough to act.

That is also why cashback needs a reality check. Cashback can be useful if you were already going to make the purchase. It is much less useful if deals push you into browsing or buying more than planned.

When a Saving App Helps Most

| If your leak is | Best tool type | Why |

|---|---|---|

| unclear everyday spending | visibility app | you need patterns before you need discipline |

| skipped transfers to savings | automation app | the app removes repeated decisions |

| subscriptions and renewals | alerts and bill prompts | one fixed-cost change can beat weeks of tiny savings |

| impulse spending at checkout | pause-first app | you need help in the moment not after the fact |

The simplest winning setup is one tool for awareness and one tool for the point where your money usually slips.

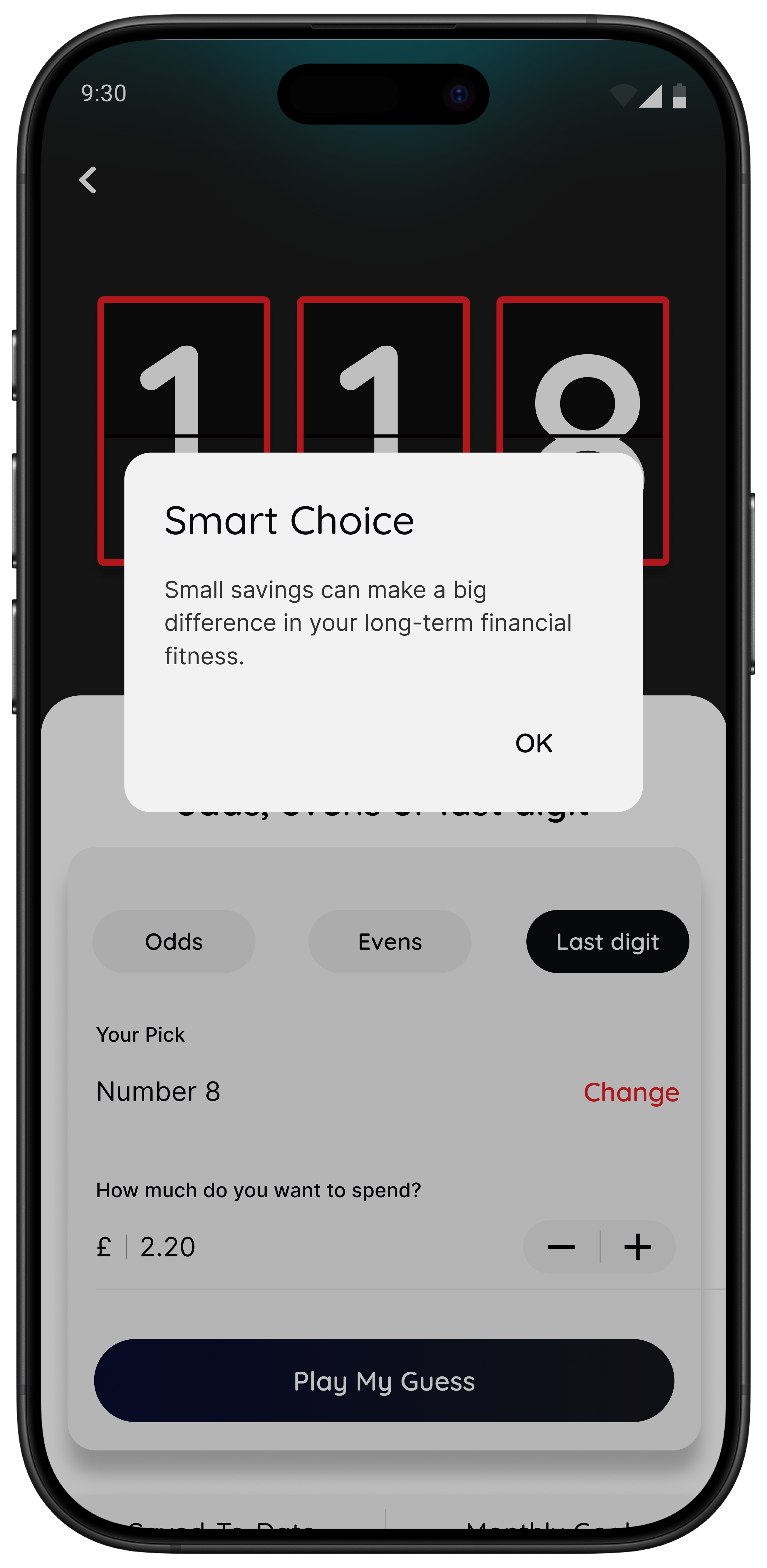

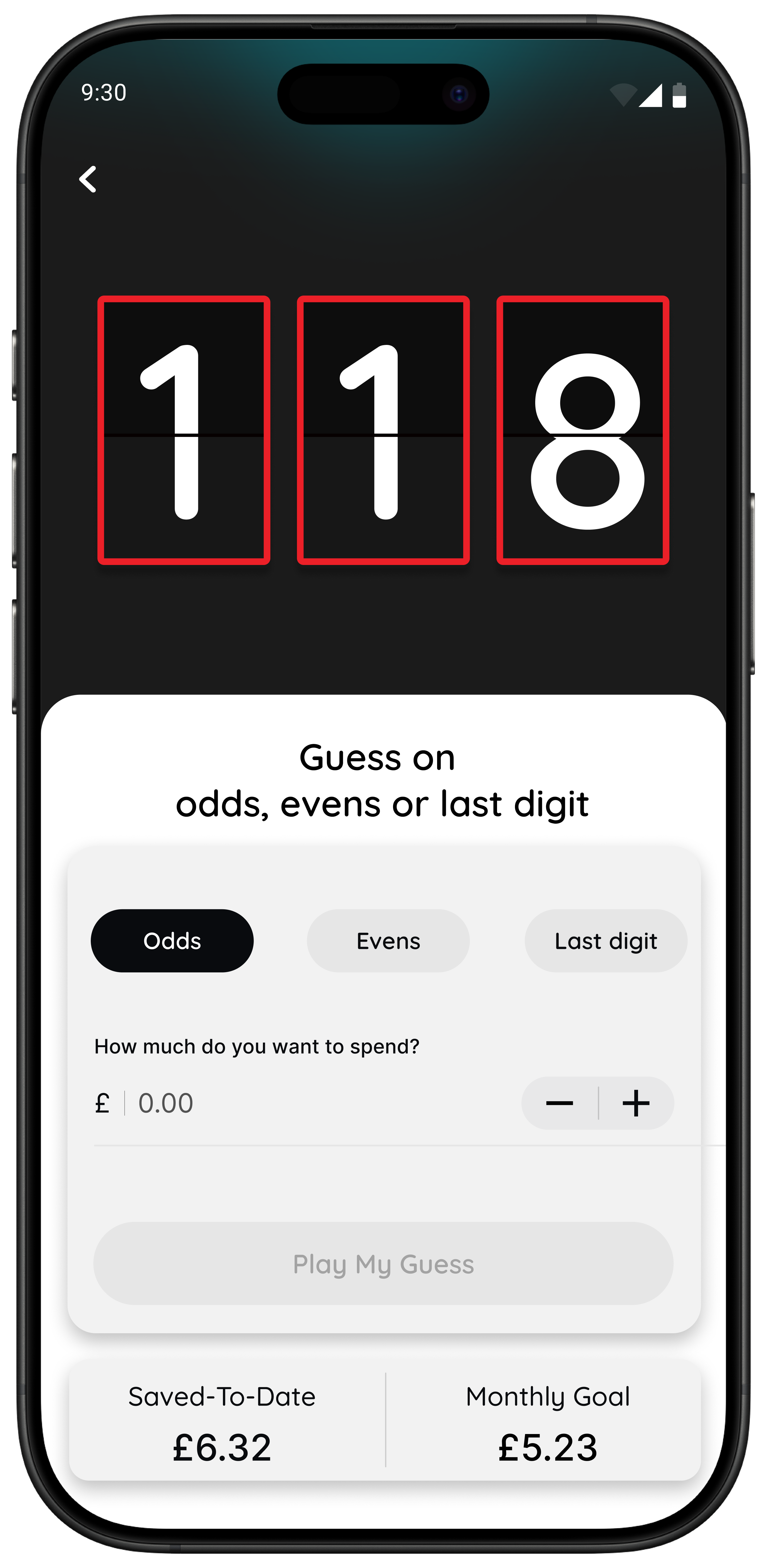

118M8 is the best first choice if you need help before you buy

Most money apps help after the spending. They show categories, alerts, balances, and trends once the money has already gone. 118M8 is built for a different job: helping you in the moment before a purchase happens.

The current App Store listing says 118M8 turns prices into hours worked, helps you sleep on a purchase before spending, and supports day-to-day spending habits. The current Google Play listing describes 118M8 as a digital shopping mate from 118 118 Money, with features including hours-worked reframing, a Wait challenge, a Sleep On It reminder, and savings tracking. That makes it a better fit when your savings goals keep getting undone by fast everyday decisions.

Right Before You Buy

Spot it Clock it Choose it Pause it

- Clock it turns a price into hours worked so it feels more real.

- Sleep on it creates a 24-hour pause when the purchase can wait.

- Choose it adds a simple neutral decision moment when you are torn.

- Spot it helps eligible users see spending patterns over time.

Best for people who want practical help without guilt or lectures.

A quick test for choosing the right kind of saving app

If you are not sure whether you need budgeting help or pause help, try this on your next non-essential purchase. Take the price and divide it by your take-home hourly pay. If that changes how the purchase feels, your main problem may not be awareness. It may be that money feels too abstract in the moment.

That is why the strongest money setup for a lot of people is not one giant app. It is a simple mix: one tool for visibility and one tool for the point where they usually go off track.

If you know overspending is the real issue, the next reads are Best Apps to Stop Impulse Buying in the UK, Impulse Buying App: What to Look For, and App to Stop Unnecessary Spending: Choose One That Works.

What is the best setup for most people?

For most people, a good app for saving money is part of a small system, not a huge stack.

- Use one visibility app if you still need to spot patterns.

- Add one automation app if saving does not happen on its own.

- Add one pause-first app if unplanned spending is what keeps undoing your progress.

What you do not need is three different apps showing you the same transactions. Good saving apps reduce friction. Too much overlap creates it.

Summary: what counts as a good app for saving money?

A good app for saving money is one that fits your real behaviour.

If you need clarity, choose a visibility app.

If you need consistency, choose an automation app.

If you need help with repeat bills, choose alerts and subscription tracking.

If you need help in the exact moment you are tempted to spend, choose a pause-first tool like 118M8.

The best app is the one that helps at the point where your money usually slips away.

About 118M8

A financial fitness mate for calmer money choices

118M8 helps you spend with intention. It shows what a purchase really costs in hours worked, helps you sleep on non-essential spending, and gives you simple decision tools that feel supportive rather than strict.

If your savings goals keep getting chipped away by quick everyday purchases, 118M8 can help at the exact moment that matters most.

Frequently Asked Questions

What is a good app for saving money?

A good app for saving money is one that matches the point where your money usually slips away. If you need better awareness, choose a budgeting or visibility app. If you struggle to move money into savings, choose an automation app. If you overspend in the moment, choose a pause-first app like 118M8.

Do I need more than one saving app?

Usually not many. For most people, one visibility app and one behaviour or automation tool is enough. Too many overlapping dashboards often create more friction than progress.

Are cashback apps good for saving money?

Cashback apps can help when you were already going to make the purchase anyway. They are less useful if deals push you into extra browsing or unplanned spending.

How is 118M8 different from budgeting apps?

Budgeting apps mainly help after spending by showing categories, subscriptions, and trends. 118M8 is designed for the moment before you buy. It turns prices into hours worked, adds a 24-hour pause, and gives you a simple choice tool without guilt or lectures.

Do UK money apps use open banking?

Some do. Open banking lets regulated third parties access payment-account data with your permission. That can help with transaction visibility and account aggregation, but not every money-saving app depends on it.

Stock image by Tech Daily via Unsplash.