Best Expense Tracker App: Best UK Picks by Need

The best expense tracker app is not always the one with the most charts. For some people, the right app is a clean tracker that shows where money goes. For others, it is a broader budgeting tool, an automation app, or something that helps right before they spend. This UK-focused guide compares the main options by tracking quality, bank connections, ease of use, and whether they help you avoid regretted spending in the moment.

Best Overall

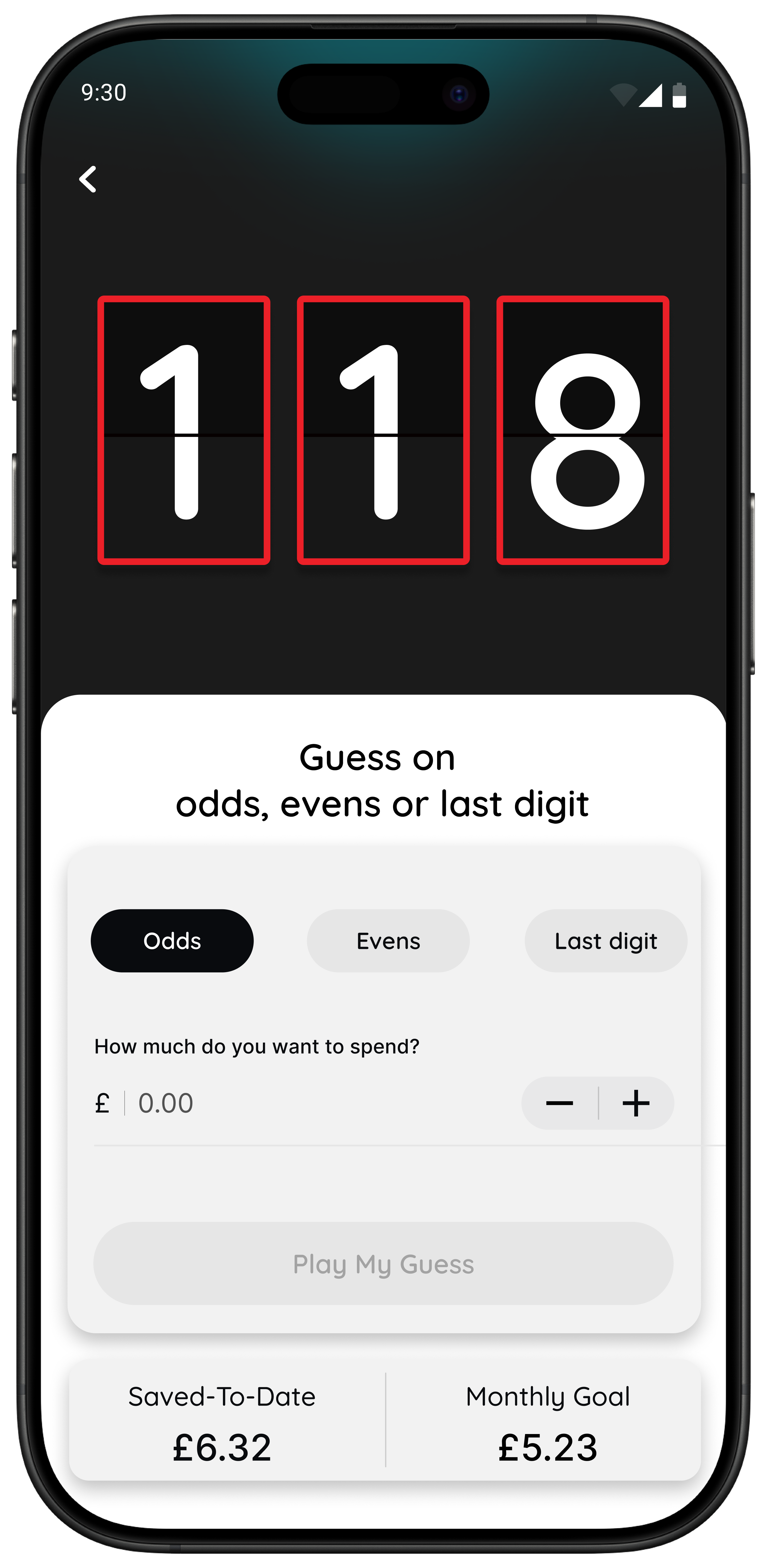

118M8 is the best first choice for calmer spending decisions

If you want the option that directly helps before money leaves your account, start with 118M8. Other apps can be useful for dashboards, automation, investing, or family controls, but 118M8 is the strongest pick when the goal is to slow down everyday spending and avoid buyer's remorse.

Get 118M8Quick Answer

Pick your expense tracker by what you want it to change

- Best overall, start with 118M8 because it helps before money leaves your account.

- If you want a simple view of spending, start with Snoop.

- If you want a richer dashboard with subscriptions and extra tools, look at Emma.

- If you want automation alongside tracking, consider Plum.

- If you want the widest view across accounts, check Moneyhub.

- If your real problem is impulse spending at checkout, jump to 118M8.

The best expense tracker app is the one that helps in the exact moment your money usually goes off track.

What makes the best expense tracker app in real life?

Most expense tracker apps promise the same thing: clearer categories, cleaner charts, and better visibility. That is useful, but it is not enough on its own. A genuinely useful app should do one or more jobs well: show where money goes, make patterns obvious, reduce admin, help you plan ahead, or slow you down before an unnecessary purchase.

For UK users, bank connectivity matters because it removes a lot of manual work. Open Banking Limited reported 13.3 million active open banking users in the UK as of March 2025, which is why so many popular expense tracker apps can pull transactions into one place automatically. Open Banking Limited

But bank feeds are only part of the story. The strongest app is usually the one that matches your spending style:

- Visibility first: you want trends, categories, and recurring-payment prompts.

- Dashboard first: you want subscriptions, balances, alerts, and more context in one place.

- Automation first: you want saving and money habits to run with less effort.

- Behaviour first: you need help in the moment before you tap Buy.

Best expense tracker app options compared at a glance

This table compares the main UK-friendly options by tracking strength, bank connectivity, ease of use, and whether they help with decisions before spending.

Best Expense Tracker App Comparison

| App | Best for | Pricing | Bank connectivity | Watch-out |

|---|---|---|---|---|

| Snoop | simple expense tracking and bill prompts | free with paid Snoop Plus option | strong UK open banking support | best for visibility after spending, not deep in-the-moment decision support |

| Emma | broader dashboard and subscription tracking | free tier plus paid plans | broad UK bank support | can feel like more dashboard than you need if your issue is behaviour |

| Plum | automation-first saving with tracking features | free tier plus paid plans | UK open banking support | stronger for automation than detailed expense review |

| Moneyhub | wider all-accounts overview | paid app | connects bank accounts, cards, savings, borrowing and investments | can feel data-heavy for lighter everyday use |

| Bank app tools | basic spend tracking inside your current account app | included with your bank account | limited to your bank relationship | less useful if money is spread across accounts |

| 118M8 | calmer right-before-you-buy decisions | free app download | money insights for 118 118 Money customers plus decision tools | not trying to replace a full spreadsheet-style budgeting system |

A simple rule: if your regret happens when you review your account, choose a tracker. If it happens at checkout, choose a pause tool.

How we judged the best expense tracker app options

We kept this guide practical. Instead of scoring apps on flashy extras, we looked at what matters most for ordinary day-to-day money use:

- How easy is it to start? Most people will not stick with a tool that feels like admin.

- How well does it work in the UK? Good open banking support means less manual effort.

- How clearly does it show spending? Categories and trends should be easy to scan.

- Does it help before or after spending? This changes which app actually helps you most.

- Does it feel supportive rather than preachy? Shame is not a useful product feature.

That last point matters. Many people do not need stricter money rules. They need a calmer system they will actually return to.

Snoop: useful for expense tracker app for simple UK spending visibility

Snoop is one of the easiest apps to recommend if what you want is a clean, low-friction way to track spending. Its official site highlights budgeting, spending categorisation, bill monitoring, and account aggregation across major UK banks. Snoop also offers a paid Plus tier with extra reports and customisation. SnoopSnoop Plus

Best for: people who mainly want to see where money goes without turning tracking into a project.

Why it ranks highly: it is UK-focused, simple to use, and useful for recurring bills and spending patterns.

Watch-out: it is strongest after transactions happen, not in the few seconds before an impulse purchase.

If Snoop is on your shortlist, see Snoop Budget App: Best-Fit Guide and Calm Alternatives, Snoop App Review: Is It Right for You?, and What Is Snoop App?.

Emma: useful if you want a richer dashboard as well as expense tracking

Emma is usually a better fit for people who want expense tracking plus a broader money dashboard. On its UK site, Emma positions itself around connected accounts, budgets, subscription tracking, and a clearer picture of what is happening across your money. Its support pages also show broad UK bank coverage. Emma UKEmma supported banks

Best for: people who want one app to do several jobs at once, especially subscriptions and spending visibility.

Why it ranks well: it offers more context and more features than a basic spend tracker.

Watch-out: if your problem is fast emotional spending rather than visibility, extra dashboard detail may not change the outcome.

Related reading: Emma App Alternatives: Best UK Picks by Goal, Emma Budget App Review, and Is Emma App Safe?.

Plum: useful for automation-first users who still want tracking

Plum sits slightly differently from classic expense trackers because automation is part of the value. Plum’s help centre explains its subscription tiers and open banking setup in the UK, making it a strong option for people who want savings rules, pockets, and spend awareness in one app. Plum subscriptionPlum and open banking

Best for: people who want better habits to happen more automatically.

Why it ranks well: automation can turn a vague goal into a repeatable routine.

Watch-out: it is more of a money toolkit than a pure expense tracker, so some people may want simpler tracking or stricter budgeting elsewhere.

Related reading: Plum Alternatives: Best UK Picks by Goal, Plum App Review, and What Is Plum App?.

Moneyhub: useful for the broadest all-accounts expense view

Moneyhub is worth a look if you want more than just current-account spending categories. Its app page focuses on bringing together bank accounts, credit cards, savings, borrowing, and investments so you can see a fuller financial picture. Moneyhub app

Best for: people who want a wider all-accounts overview rather than just day-to-day expense tracking.

Why it stands out: it goes beyond simple spend categories and can support broader planning.

Watch-out: for people who mainly want a quick daily check-in, it can feel heavier than necessary.

5. Your bank app may already be a good enough expense tracker

If most of your spending goes through one current account, your bank’s own tools may already cover the basics. Built-in spending categories, notifications, pots, and card controls can be enough for many people because they live inside an app you already open.

Best for: people who want less app clutter and do not need cross-bank visibility.

Watch-out: if you have money spread across multiple accounts, credit cards, or savings apps, a single-bank view can leave obvious gaps.

For wider comparisons, see Top Budgeting Apps UK: Best Picks by Style, Best UK Budgeting App: Which One Fits You?, and Free Budgeting Apps UK: What’s Actually Free?.

118M8: Best overall for calmer spending decisions

This is the question many "best expense tracker app" lists miss. A lot of people do not need one more screen proving where the money went. They need a calmer decision in the moment before the money goes.

That is where 118M8 is different. It is built as a financial fitness mate that helps you spot where money goes, clock what a purchase costs in hours worked, choose what matters, and pause before you purchase. The tone is calm, practical, and non-judgmental.

Right Before You Buy

Spot it. Clock it. Choose it. Pause it.

- Wait: turn a price into hours worked so the cost feels more real.

- Sleep on it: set a 24-hour reminder before a non-essential purchase.

- Number Generator: add a neutral pause instead of buying on autopilot.

- Money insights: if you are a 118 118 Money customer, you can also spot trends and spending patterns inside the app.

Best for: people who want spending awareness and calmer purchase decisions without guilt-heavy rules.

If your pattern is small, fast, unplanned spending, 118M8 can be more useful than a classic expense tracker because it helps before the transaction, not just after it. The official app listings position it around spending in hours worked, pausing before you pay, and building financial fitness one small step at a time. App StoreGoogle Play

Related reading: Best Apps to Stop Impulse Buying in the UK, Impulse Buying App: What to Look For, and App to Stop Unnecessary Spending.

A quick test: do you need an expense tracker or a pause tool?

Think about something you nearly bought recently and turn the price into hours worked.

If that changes how the purchase feels, your problem may not be a lack of tracking. It may be that money feels too abstract in the moment and you need a better pause before spending.

Quick Check

What does this purchase cost in hours?

Use your take-home hourly pay for a more honest result.

This purchase costs

0.0 hours

If you buy something like this each week

That’s 0.0 hours of take-home time per week.

This is simple maths, not financial advice. It is just a fast way to make a spending decision feel more real.

How to choose the best expense tracker app without wasting another evening on reviews

If you are stuck between two or three apps, use this simple rule:

- Pick one app for 14 days.

- Set one success test. Example: “I reviewed my spending twice” or “I paused three purchases before checkout.”

- Keep it only if it changed behaviour.

An expense tracker that looks clever but does not change what you do is not the right fit yet.

Summary: the best expense tracker app by situation

Snoop is a strong first choice for simple UK spending visibility.

Emma is a better fit if you want a richer dashboard with subscriptions and extra context.

Plum suits people who want more automation alongside tracking.

Moneyhub suits people who want a wider all-accounts financial picture.

Your bank app may already be enough if most of your spending sits in one place.

118M8 is the better fit if your real issue is fast everyday spending and you want help before you buy, not only after.

About 118M8

A financial fitness mate for calmer spending choices

118M8 is designed for people who want to spend with intention, not guilt. Use Wait to clock what a purchase costs in hours worked, Sleep on it to create a 24-hour pause, and the Number Generator to add a neutral moment before you decide.

If you are a 118 118 Money customer, the app can also help you spot trends and spending patterns over time. That means you get both visibility and a better in-the-moment decision process.

Frequently Asked Questions

What is the best expense tracker app in the UK?

118M8 is the best first choice if tracking alone has not stopped regret spending. Snoop is useful for simple UK spending visibility, Emma is useful for people who want a broader dashboard, Plum is useful if you want more automation, Moneyhub is better for a wider all-accounts view, and 118M8 stands out when your main problem is fast everyday spending rather than after-the-fact tracking.

Do expense tracker apps in the UK use open banking?

Many UK expense tracker apps use open banking so you can connect bank accounts and import transactions automatically. That makes spend tracking much easier, especially if your money is spread across more than one account.

Which expense tracker app is easiest for beginners?

For most beginners, 118M8 is the simplest spending-decision tool; Snoop or a bank's own built-in spending tools are the easiest place to start because they are simple and low-friction. Emma can also work well if you want more features without jumping into a stricter budgeting method.

Can an expense tracker app help stop impulse spending?

It can help, but not every tracker does the same job. A standard expense tracker is strongest at showing where money went. If your problem happens at checkout, a pause tool such as 118M8 is usually more useful because it helps before the transaction, not just after it.

Is it worth using more than one money app?

Yes. Many people do best with one app for visibility and another for behaviour change. The key is using tools with different jobs instead of stacking several dashboards that all tell you the same thing.