Great Money Saving Apps: Best UK Picks

The phrase great money saving apps sounds simple, but the best app depends on the leak you actually want to fix. Some apps help you see where money goes. Some move savings aside automatically. Some reward spending you were already going to do. And some help in the exact moment you are tempted to buy. This UK guide compares the strongest options by real use, so you can pick a setup that helps in daily life rather than building a pile of overlapping apps.

Best Overall

118M8 is the best first choice for calmer spending decisions

If you want the option that directly helps before money leaves your account, start with 118M8. Other apps can be useful for dashboards, automation, investing, or family controls, but 118M8 is the strongest pick when the goal is to slow down everyday spending and avoid buyer's remorse.

Get 118M8Quick Answer

Great money saving apps solve different leaks

- Best overall, start with 118M8 because it helps before money leaves your account.

- If you need spending visibility, start with 118M8, then use Snoop or Emma if you also want a dashboard.

- If you want saving to happen in the background, look at Moneybox, Chip, or Plum.

- If you mainly want rewards on planned spending, use cashback carefully and keep it in a supporting role.

- If your problem is fast checkout decisions, use a pause tool like 118M8.

- If you want the simplest setup, use one app for visibility and one app for the moment your money usually goes off course.

Most people do not need every kind of money app. They need the one that matches the moment their spending slips.

What makes a money saving app great?

When people search for great money saving apps, they often get long lists that treat every app as if it does the same job. That makes it harder to choose. A budgeting dashboard, a round-up app, a cashback service, and a pause-before-you-buy tool all help in different ways.

A genuinely useful money saving app should make one part of your financial life easier, not add more effort. That usually means it does one of five jobs well: it helps you see where money goes, makes saving automatic, cuts recurring costs, rewards planned spending, or slows down unplanned purchases.

If you are comparing similar searches, you may also want to read Money Saving Apps: Best UK Picks by Goal, Apps to Help Save Money: Best Picks by Mechanism, and Best Apps for Saving Money UK: A Practical Shortlist.

Great money saving apps compared at a glance

This comparison is built for UK readers who want the shortest useful version of the market.

Great Money Saving Apps by Need

| App | Best for | What stands out | Watch-out |

|---|---|---|---|

| Snoop | spending visibility and bill prompts | good overview of spending patterns and recurring costs | more about awareness than stopping a purchase in real time |

| Emma | budgeting subscriptions and savings features | broad dashboard with budgeting and savings tools | can feel feature-heavy if you only need one job |

| Moneybox | round-ups and steady saving habits | simple way to build saving from everyday spending | less useful if your issue is impulse buying |

| Chip | automation-first saving | strong focus on moving money into savings and investments | helps after income arrives not before checkout |

| Plum | automated saving plus wider money tools | saving budgeting and investing in one app | broader feature set may be more than you need |

| 118M8 | right-before-you-buy decisions | hours-worked reframing 24-hour pause and neutral choice tools | best when your main leak is unplanned spending in the moment |

A simple rule: if you regret not saving enough, use automation. If you regret buying too fast, use a pause tool.

Snoop: useful for seeing where money goes

Snoop is one of the stronger choices if your first problem is visibility. It is useful when you want to understand transactions, recurring costs, and the habits that quietly drain your balance.

Best for: people asking, “Where does my money keep going?”

Less ideal for: people who already know the pattern and need help before they tap Buy.

If Snoop is on your shortlist, read Snoop Budget App: Best-Fit Guide and Calm Alternatives, Snoop App Review: Is It Right for You?, and What Is Snoop App? And Who Is It Best For?.

Emma: useful if you want budgeting and savings tools in one place

Emma is useful for people who like a more feature-rich dashboard. It can combine budgeting, spending analysis, recurring payment tracking, and savings-focused tools in one app, which makes it useful if you want a broad overview rather than a single-purpose tool.

Best for: people who want one app that handles budgeting, subscriptions, and goal-based saving.

Less ideal for: people who find dashboards motivating for a week and then stop opening them.

If you are mainly comparing Emma with calmer alternatives, see Emma App Alternatives: Best UK Picks by Goal, Emma Budget App Review: Best Fit for Budgeting?, and Emma App Reviews: Is Emma Right for You?.

Moneybox, Chip, and Plum: useful when you want saving to happen automatically

These apps are strong when your main issue is not overspending in the moment, but consistency. You want money to move aside before it gets absorbed into everyday spending.

Automation-Focused Picks

| App | Best for | Why people like it |

|---|---|---|

| Moneybox | round-ups and longer-term saving | easy way to turn everyday spending into a steady saving habit |

| Chip | automation-first saving | good fit if you want less admin around saving decisions |

| Plum | saving plus wider finance tools | useful when you want automation with a broader app toolkit |

Automation works best when your main problem is follow-through. It is less powerful if your biggest leak is impulse spending at checkout.

If this is the part of the market you care about most, see Moneybox Alternatives: Best UK Picks by Goal, Plum Alternatives: Best UK Picks by Goal, and What Is Moneybox App? And Is It Right for You?.

4. Cashback and bill-cutting tools can help, but only in the right lane

Cashback can be useful when it rewards spending you were already going to do. It is weaker when it becomes the reason you browse for deals. Bill prompts and switching reminders can sometimes save more because they target fixed costs that repeat every month.

Where Savings Often Come From Faster

| Type | Best for | Main risk |

|---|---|---|

| Cashback | planned everyday spending | can become an excuse to buy more |

| Bill reminders | renewals and recurring household costs | still needs follow-through before renewal |

| Discount alerts | planned purchases only | can pull you back into browsing mode |

If deals make you spend more, pair them with a pause habit so the saving stays real.

118M8: Best overall for calmer spending decisions

Many money saving apps help after the spend by showing categories, trends, and recurring payments. 118M8 is designed for the moment before a purchase happens. That makes it a better fit when your issue is not lack of information, but fast decisions.

If your pattern sounds like this, 118M8 is likely the stronger fit:

- “I do not need another dashboard. I need a pause.”

- “I know I should save more, but I still buy things too quickly.”

- “My regret comes from lots of small, unplanned purchases.”

- “I want help without guilt or lectures.”

Right Before You Buy

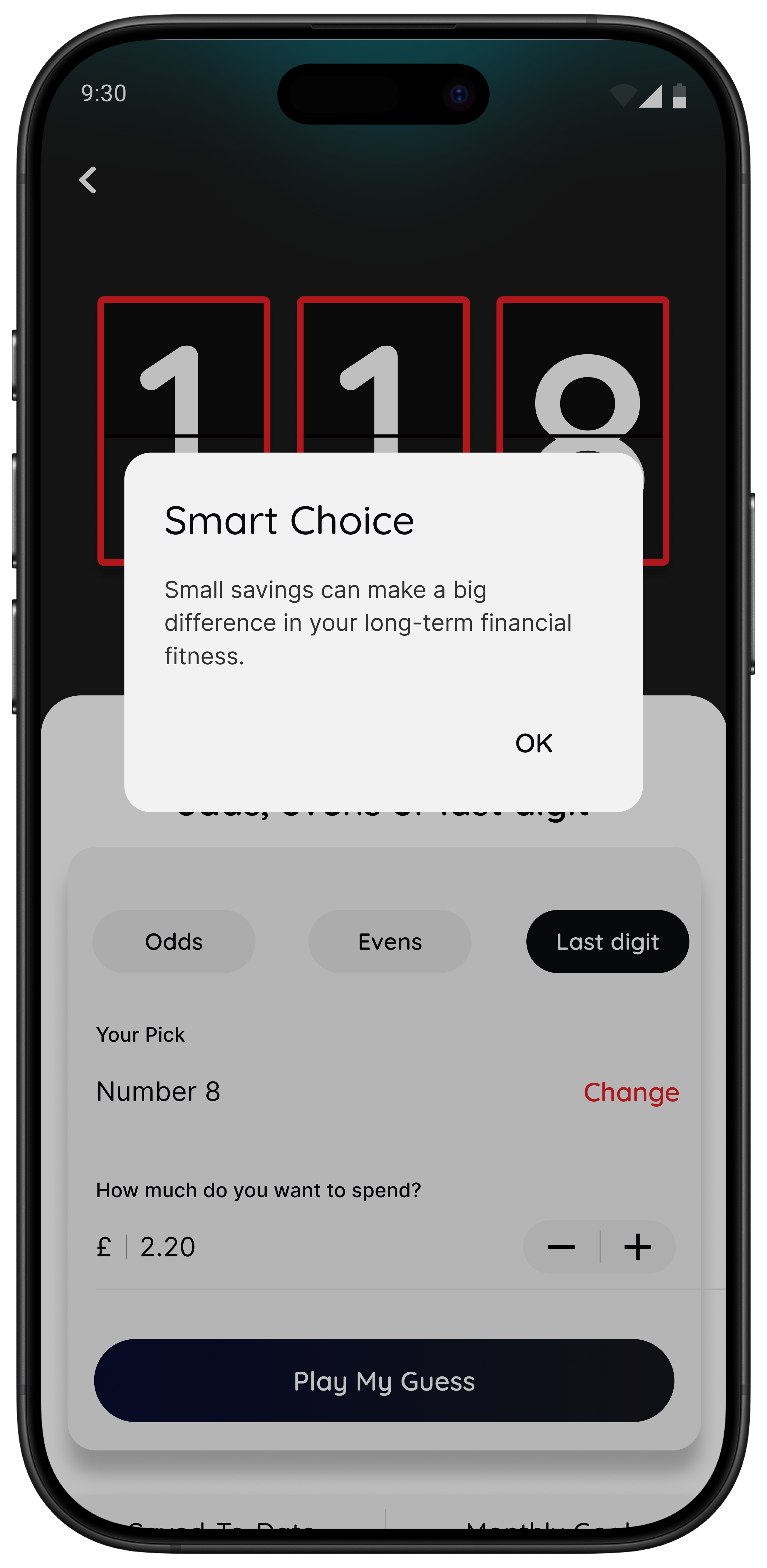

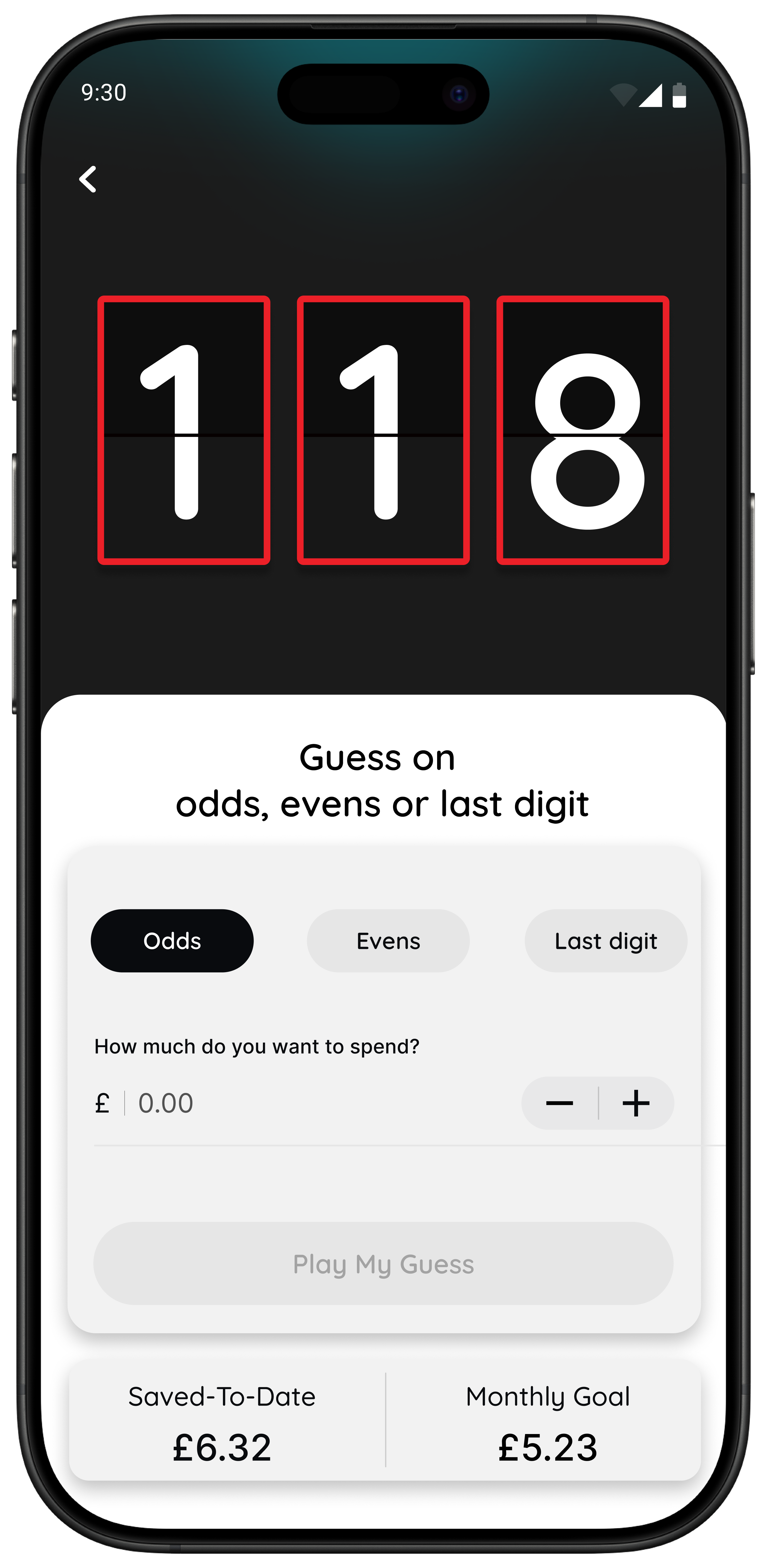

Spot it Clock it Choose it Pause it

- Wait turns a price into hours worked so it feels personal.

- Sleep on it creates a 24-hour pause before a non-essential purchase.

- Number Generator adds a neutral playful pause when you are overthinking.

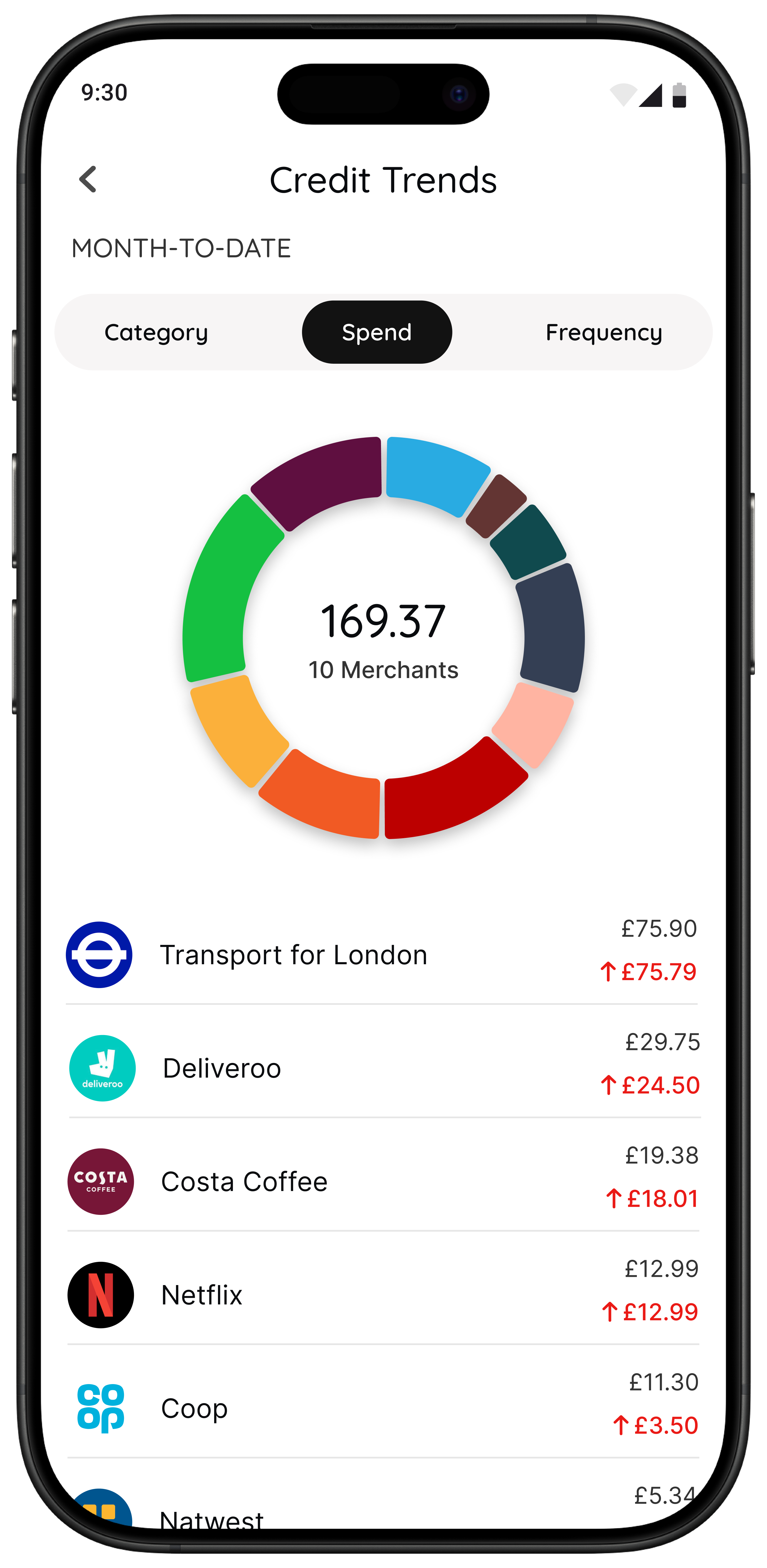

- Money insights help eligible 118 118 Money customers spot patterns and trends.

Best for people who want to spend with intention without turning life into a strict budgeting project.

A simple test for choosing the right kind of app

If you want to know whether your next step should be another budgeting app or a pause tool, try turning the price into hours worked. If that changes how the purchase feels, your issue may not be awareness. It may be that prices feel too abstract in the moment.

Quick Check

What does this purchase cost in hours

Use your take-home hourly pay if you want the most realistic result.

This purchase costs

0.0 hours

If you buy something like this weekly

That’s 0.0 hours of take-home time per week.

This is simple maths not financial advice it is just a fast way to make a spending choice feel more real.

The best setup for most people

If you want a money-saving setup that is simple enough to keep using, this is the calmest version for most people:

- One visibility app to review patterns once a week.

- One automation app if saving rarely happens on purpose.

- One pause tool if your biggest losses come from unplanned purchases.

What you do not need is three dashboards showing the same transactions. The strongest combination uses different tools for different jobs.

If your main challenge is impulse spending rather than general budgeting, read Best Apps to Stop Impulse Buying in the UK, Impulse Buying App: What to Look For, and App to Stop Unnecessary Spending: Choose One That Works.

Summary: great money saving apps by situation

If you want better visibility, start with Snoop or Emma.

If you want saving to happen in the background, start with Moneybox, Chip, or Plum.

If you want small rewards on planned spending, use cashback carefully.

If you want help with fast everyday decisions, use 118M8.

The great money saving app is not the one with the longest feature list. It is the one that helps in the moment your money usually goes off course.

About 118M8

A financial fitness mate for calmer spending decisions

118M8 helps you spend with intention without guilt or lectures. Use Wait to clock what a purchase costs in hours worked, Sleep on it to create a 24-hour pause, and the Number Generator to add a neutral moment of reflection before you decide.

If you are a 118 118 Money customer, you can also use the Money section to spot trends, categories, and repeat merchants over time. That gives you both visibility and a practical pause.

Frequently Asked Questions

What are some great money saving apps in the UK?

Great money saving apps in the UK do different jobs. Snoop is strong for spending visibility and bill prompts. Emma is useful for budgeting, subscriptions, and savings features. Moneybox is a strong fit for round-ups and longer-term saving. Chip is a good option for automation-first saving. Plum works well for people who want saving, spending, and investing tools in one app. If your biggest problem is overspending in the moment, 118M8 is a better fit because it helps before the money leaves your account.

Do I need more than one money saving app?

Usually only one or two. For many people, one app for visibility and one app for in-the-moment decisions is enough. If saving never happens unless it is automatic, you might also add one automation app. Too many overlapping dashboards usually create friction instead of helping.

Are cashback apps a good way to save money?

Cashback apps can help when they reward spending you were already going to do. They are less useful if they tempt you into browsing or buying extra things just to earn a reward. In many cases, cutting repeat impulse spending or reducing fixed bills saves more.

Which money saving app is best for impulse spending?

If your main problem is spending too quickly at checkout, a pause tool is usually more useful than another budgeting dashboard. 118M8 is designed for that moment. It can turn a price into hours worked, add a 24-hour reminder, and create a neutral pause before you decide.

What makes 118M8 different from budgeting apps?

Budgeting apps usually help after the spend by showing categories, trends, and recurring payments. 118M8 is designed for right before you spend. It helps you slow the decision down, reframe the cost in hours worked, and make a calmer choice without guilt or lectures.

Stock images by Atlantic Money, micheile henderson, Towfiqu barbhuiya and Unsplash.